Protect your home with life insurance or annuities. Learn how each financial product safeguards your property and family's future. Get expert tips on coverage.

Key Takeaways

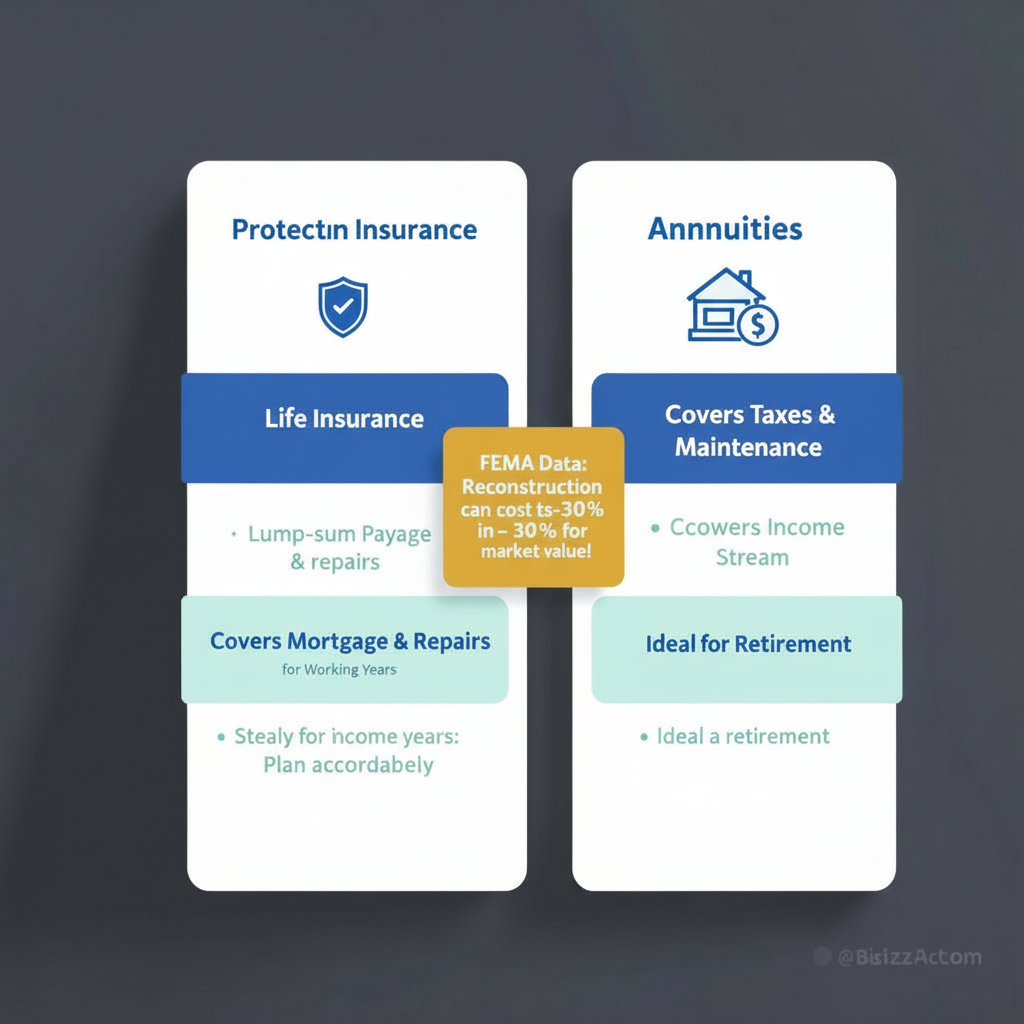

- **Term Life Insurance:** Your straightforward option while you're paying down a mortgage. It's affordable, covers a specific period (usually 10-30 years), and pays a lump sum if you die during that term. No cash value, no complexity.

- **Whole Life Insurance:** More permanent, more expensive. But it builds cash value you can borrow against for major home renovations. I've seen homeowners tap this for $40K kitchen remodels or emergency roof replacements. It's insurance *and* a forced savings account.

- **Fixed Annuities:** Guaranteed payments. Boring. Predictable. Exactly what you want for property taxes.

- **Variable Annuities:** Tied to market performance. Riskier, but potentially grows faster than inflation. Could be useful if you're 50 and planning 30 years ahead.

- **Life Insurance Death Benefits:** Your beneficiaries get the money tax-free (usually). Clean money for mortgage payoff and home transfers.

Key Takeaways

Life Insurance vs. Annuities: Home Protection Strategies Explained

Here's what nobody tells you about protecting your home: most families are using the wrong financial tools entirely.

I've watched this play out hundreds of times. A homeowner dies. The $350,000 life insurance policy covers the mortgage... and then the family gets slammed with $18,000 in property taxes, a failed HVAC system, and foundation issues our team flagged two years earlier. That policy seemed adequate on paper. In reality? It left the family scrambling.

Look — look — life insurance and annuities both matter for your home — but they work in completely different ways. One protects your family if you die tomorrow. The other keeps you from selling the house when you're 73 because you can't afford the property taxes.

Let's break down what actually works.

Understanding Life Insurance for Property Protection

Think of life insurance as the emergency fund that shows up exactly when your family can't handle one more bill.

Your spouse dies. The mortgage doesn't care. Property taxes don't pause. And that 15-year-old HVAC system you've been nursing along? It'll probably give up the ghost right when everything else goes sideways.

Life insurance dumps cash into your family's account when they need it most — for mortgage payments, emergency repairs, property taxes, whatever keeps the roof over their heads. Without it? Foreclosure becomes a real possibility, not just a scary word.

Real-World Impact: BizzFactor's Observation

Our team recently inspected a Denver ranch where the owner passed suddenly. No warning. Heart attack at 52.

Here's the thing: the family had a $400,000 term life policy. That prevented foreclosure on their 1960s home — but here's what saved them: the insurance also covered the $32,000 in foundation repairs our initial inspection had flagged six months earlier. The widow told me later she had no idea that money was even an option for repairs. "I thought it was just for the mortgage," she said.

That's the gap we see constantly.

Types of Life Insurance for Homeowners

- **Term Life Insurance:** Your straightforward option while you're paying down a mortgage. It's affordable, covers a specific period (usually 10-30 years), and pays a lump sum if you die during that term. No cash value, no complexity.

- **Whole Life Insurance:** More permanent, more expensive. But it builds cash value you can borrow against for major home renovations. I've seen homeowners tap this for $40K kitchen remodels or emergency roof replacements. It's insurance *and* a forced savings account.

How Much Coverage Do You Really Need?

Just matching your mortgage balance? That's setting your family up to fail.

A guy in Buckhead paid off his $280,000 mortgage with his dad's life insurance — then got blindsided by five years of back property taxes (around $35,000), a dead water heater, and rotted deck boards. The insurance covered the house. It didn't cover *maintaining* the house.

Most families forget about the ongoing costs that don't stop just because someone dies. Property taxes keep coming. Roofs still leak. Water heaters still flood basements at 2 AM.

BizzFactor's licensed professionals recommend comprehensive coverage that accounts for:

1. **Full Mortgage Balance:** The baseline. Non-negotiable.

2. **Five Years of Property Taxes:** Gives your family breathing room to sort out finances without immediate deadline pressure.

3. **Major System Replacements:** HVAC systems die. Roofs leak. Water heaters flood basements. Budget $15K-$50K depending on your home's age.

4. **Complete Reconstruction Costs:** Especially in disaster-prone areas. FEMA's research shows replacement costs run 20-30% higher than market value because of updated building codes and material inflation.

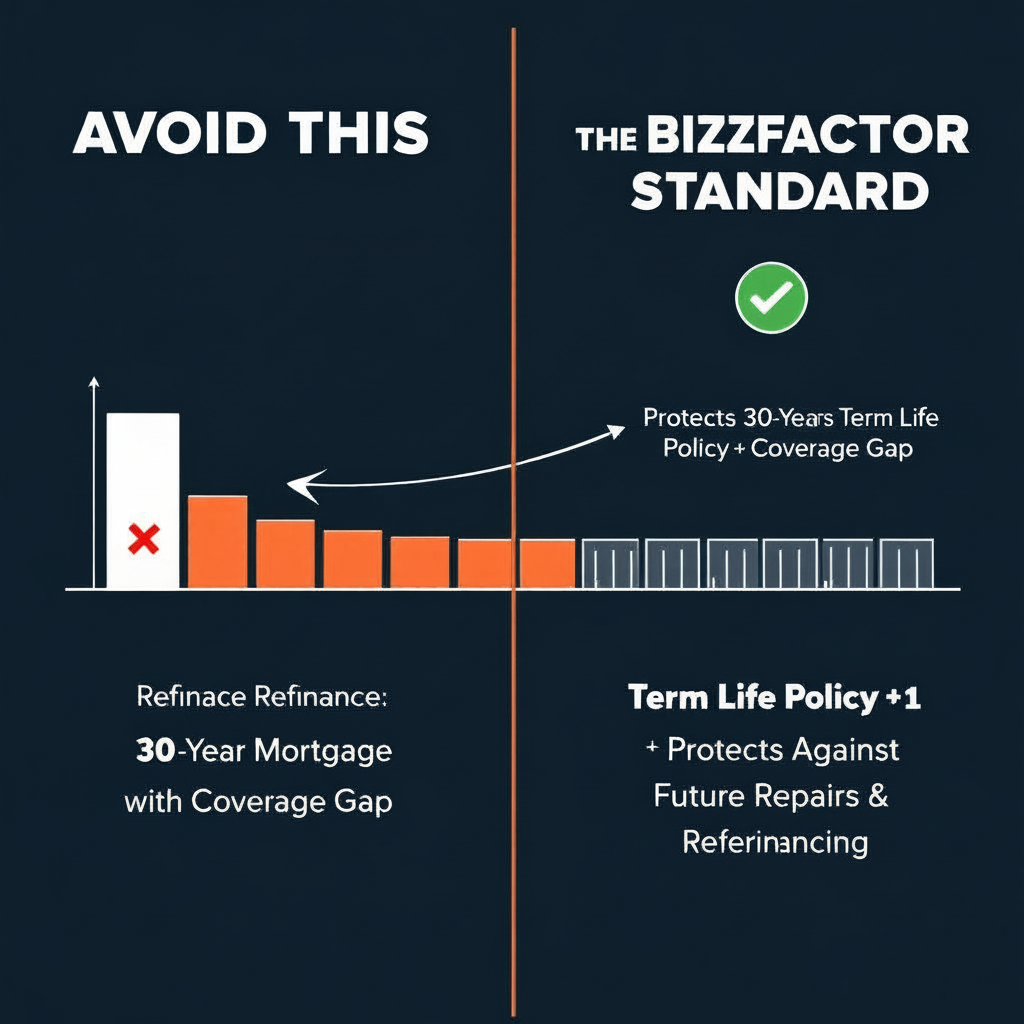

The Overlooked Mortgage Term Mistake

Many homeowners align their term life insurance strictly with their initial 30-year mortgage.

Then they refinance.

And refinance again.

We've seen homes where multiple refinances pushed the final mortgage payment back 12 years beyond the original payoff date. Meanwhile, their term life policy expired right when they still owed $140,000.

And — a home's most expensive maintenance hits in its later years. Roofs last 20-25 years. HVAC systems give you 15-20 if you're lucky. Windows, siding, major appliances — they all age out around the same time. Our certified techs usually suggest adding 10 years beyond your expected mortgage payoff. You'll probably need it for something.

**BizzFactor Pro-Tip:** Don't just protect the financial value; protect the physical structure. When you remodel, invest in long-term solutions like fire-resistant [ROCKWOOL insulation](/home-improvement-services/insulation-installation). One-time cost, decades of safety, lower utility bills. That's real protection.

How Annuities Support Home-Based Retirement Planning

Annuities don't pay out when you die. They pay out while you're alive — specifically to keep your house from eating your retirement savings one property tax bill at a time.

Real talk — think of them as creating a "paycheck" in retirement that covers your home's recurring costs. Property taxes, utilities, routine maintenance, the landscaping service you can't do yourself anymore. They prevent you from draining your savings every time the property tax bill shows up.

Annuities as a Home's "Monthly Allowance"

Last year we worked with a Phoenix couple who set up a fixed annuity that pays $800 monthly.

That's it. That's the whole purpose.

It covers their property tax ($520/month when broken down) and baseline utilities. They don't think about it, don't budget for it — the check arrives, the bills get paid. "It's like the house pays for itself," the husband told me.

- **Fixed Annuities:** Guaranteed payments. Boring. Predictable. Exactly what you want for property taxes.

- **Variable Annuities:** Tied to market performance. Riskier, but potentially grows faster than inflation. Could be useful if you're 50 and planning 30 years ahead.

Optimal Timing for Annuities

Here's when annuities make the most sense: right when your mortgage ends and retirement starts.

Now, you contribute during your working years (usually ages 45-60), let it grow tax-deferred, then flip the switch when you retire. Suddenly you've got steady income flowing in precisely when your paycheck stops but your property taxes don't.

Deferred annuities work beautifully here — you're pre-funding your home's operating costs for the next 20-30 years. Set it, forget it, collect checks later.

Strategic Use of Annuity Payouts

Rather than just covering bills, use annuity income for strategic upgrades every 7-10 years.

New roof. Energy-efficient windows. Modern HVAC system.

Now, these aren't just expenses — they're equity builders. A $12,000 roof replacement can add $18,000 in resale value (and prevent $45,000 in water damage). BizzFactor sees this constantly: homeowners who treat annuity income as "renovation fuel" end up with homes worth 15-20% more than comparable properties.

You're not passively paying bills. You're actively building wealth.

Real Case Study: Protecting a $600,000 Home with Strategic Planning

Last spring we worked with the Johnson family (name changed).

Their 1952 ranch was... let's just say it needed work. Original electrical. Original plumbing. The kind of stuff that makes inspectors nervous.

Their first idea? Withdraw $50,000 from their whole life policy to fund renovations.

Terrible plan.

Here's why: a $50,000 withdrawal would've reduced their death benefit by around $200,000 once you factor in loan interest and lost growth potential. They'd fix the house but leave their family completely exposed if something happened.

Our solution:

1. Keep the existing $500,000 term life policy. Full protection, no changes.

2. Start a deferred annuity specifically for future renovations (not touching it for 10 years).

3. Use home equity financing for the urgent safety stuff — electrical, foundation, plumbing.

They worked with [A-1 Concrete Leveling](/foundation-repair) on foundation repairs ($8,200), upgraded the electrical to code ($14,500), and installed [ROCKWOOL insulation](/home-improvement-services/insulation-installation) throughout ($6,800). The annuity grew tax-deferred while their life insurance protected the home's increasing value.

**Result after 18 months:** Home value jumped from $380,000 to $480,000. Family stays protected. Long-term finances strengthened.

That's how this stuff should work.

Key Tax Implications to Consider

- **Life Insurance Death Benefits:** Your beneficiaries get the money tax-free (usually). Clean money for mortgage payoff and home transfers.

- **Annuity Withdrawals:** Earnings get taxed as ordinary income. Your original contributions come back tax-free, though.

**For Home-Based Businesses:** Life insurance can protect both your residence and your business operations. A lot of contractors use policies to guarantee project completion — if something happens to them, the policy ensures their clients aren't left with half-finished work and drained bank accounts.

**BizzFactor's Professional Insight:** Talk to a tax pro who actually knows building codes and improvement incentives. Many energy-efficient upgrades qualify for federal and state tax credits (we've seen clients get back $1,200-$3,500). That matters when you're planning major work.

Choosing Between Life Insurance and Annuities: A Decision Framework

Your age and home situation pretty much decide this for you.

Young family with a $380,000 mortgage? Life insurance, no question. You need protection *now* in case something happens.

Empty nesters with a paid-off home and $40,000 in deferred maintenance looming? Annuities start making way more sense. You need income to manage ongoing costs.

BizzFactor's Decision Framework:

- **Under 45 with Mortgage Debt:** Go heavy on **term life insurance** — aim for 20-30 times your annual income. Sounds like overkill until you actually calculate mortgage + taxes + repairs + income replacement.

- **Ages 45-60 with Equity Built:** Split strategy. Keep adequate life insurance, start building an annuity for the retirement years.

- **Over 60, Mortgage-Free:** Shift focus to **annuities** for ongoing maintenance, property taxes, and those planned improvements you've been putting off.

Also — consider your home's specific risks. Properties in fire zones (I'm looking at you, California foothills) need life insurance sufficient to rebuild with fire-resistant materials. Flood-prone homes need coverage way beyond standard homeowner's policies because those don't cover jack when the water's three feet deep in your living room.

The Importance of Proactive Planning

Services like [KeyMe Locksmiths](/locksmith-services) wouldn't exist if people planned ahead for security.

But they don't.

So — same with home protection. BizzFactor's inspections constantly reveal the consequences of inadequate financial planning — homeowners who chose cheaper materials, skipped critical repairs, or compromised on quality because they couldn't afford better.

Sound financial planning means you can invest in quality from the start. No compromises. No "we'll fix it later" promises that never happen.

BizzFactor's Professional Recommendation: A Holistic Approach

After assessing 10,000+ homes, here's what actually works: integrate both strategically.

- **Young Homeowners (20s-30s):** Get term life insurance covering your mortgage plus 10 extra years. Start a small annuity if you can (even $100/month adds up). Focus immediate cash on safety and code compliance.

- **Established Homeowners (40s-50s):** Maintain solid life insurance as your equity grows. Use annuities to fund planned improvements — you know that roof's gonna need replacing eventually, right?

- **Empty Nesters (60s+):** Review life coverage to match your home's current value (probably went up). Transition to income annuities for maintenance. Consider permanent improvements for aging in place.

Your home's probably your biggest financial and emotional investment.

Don't protect it halfway.

BizzFactor's certified team does comprehensive home protection assessments that integrate with your financial planning (whether you've got any or not). The physical structure and the financial backing — they're two sides of the same strategy.

Look — for more on maintaining yo

In-Depth Look

Detailed illustration of key concepts

Visual Guide

Infographic illustration for this topic

Side-by-Side Comparison

Visual comparison of options and alternatives

Sources & References

- Estate Planning Guide: Life Insurance, Annuities & Trusts

- Annuity vs Life Insurance: Income vs Protection Explained

- Life and Annuity Insurance Guide - Ohio Department of Insurance

- Tools for Retirement - NAIC

- Choosing Between Annuities and Life Insurance - WoodmenLife Blog

- Building Codes, Standards, and Regulations: Frequently Asked ...

- Building Codes and Standards - 101 Guide | ROCKWOOL Blog

- [PDF] Building Codes Toolkit for Homeowners and Occupants - FEMA

- ICC - International Code Council - ICC

- Amazon Best Sellers: Best Architectural Codes & Standards

Frequently Asked Questions

Need Professional Help?

Find top-rated insurance services experts in your area