Contractors face unique risks. This 2024 guide provides essential protection insights, revealing why most are underinsured and how to choose the best life insurance for home service professionals.

Key Takeaways

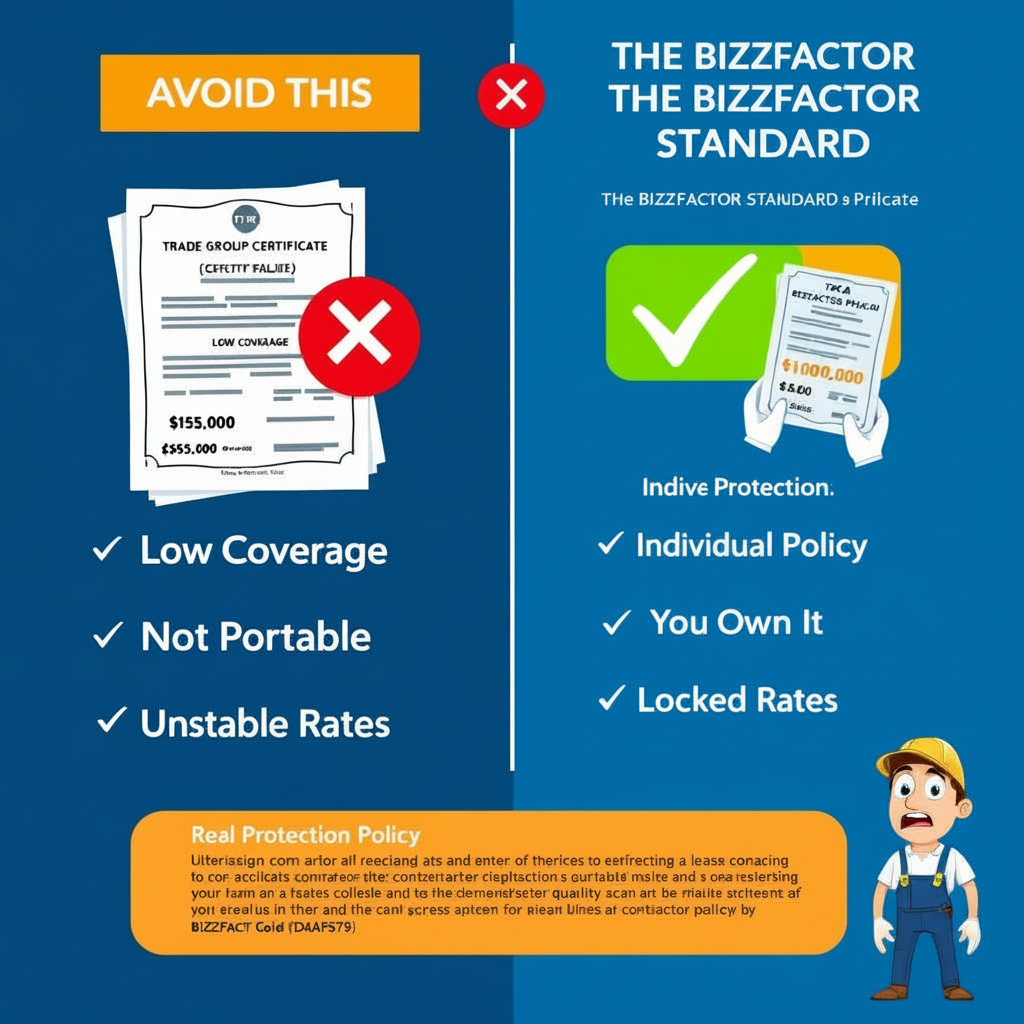

- **Low Coverage Limits:** Frequently capping under $50,000.

- **Non-Portability:** Coverage typically terminates if you switch associations or employers.

- **Unpredictable Rates:** Premiums can increase without prior notice.

- **Lack of Control:** You have minimal say over policy terms and conditions.

- **Lower Premiums:** Often 80% less expensive than comparable whole life policies.

Key Takeaways

Life Insurance for Contractors 2024: The Essential Protection Guide for Home Service Professionals

A guy I know in Buckhead spent three years thinking his trade association policy had him covered. When he died last spring — freak accident involving a ladder and a power line — his wife got a check for $15,000. Didn't even cover the funeral.

If you're swinging hammers, running wire, or climbing roofs for a living, your life insurance situation is nothing like some marketing director's. The risks are different. The coverage needs are different. And yeah, the insurance companies treat you differently too.

Why Life Insurance Is Non-Negotiable for Home Services Professionals

Contractors get hurt. A lot.

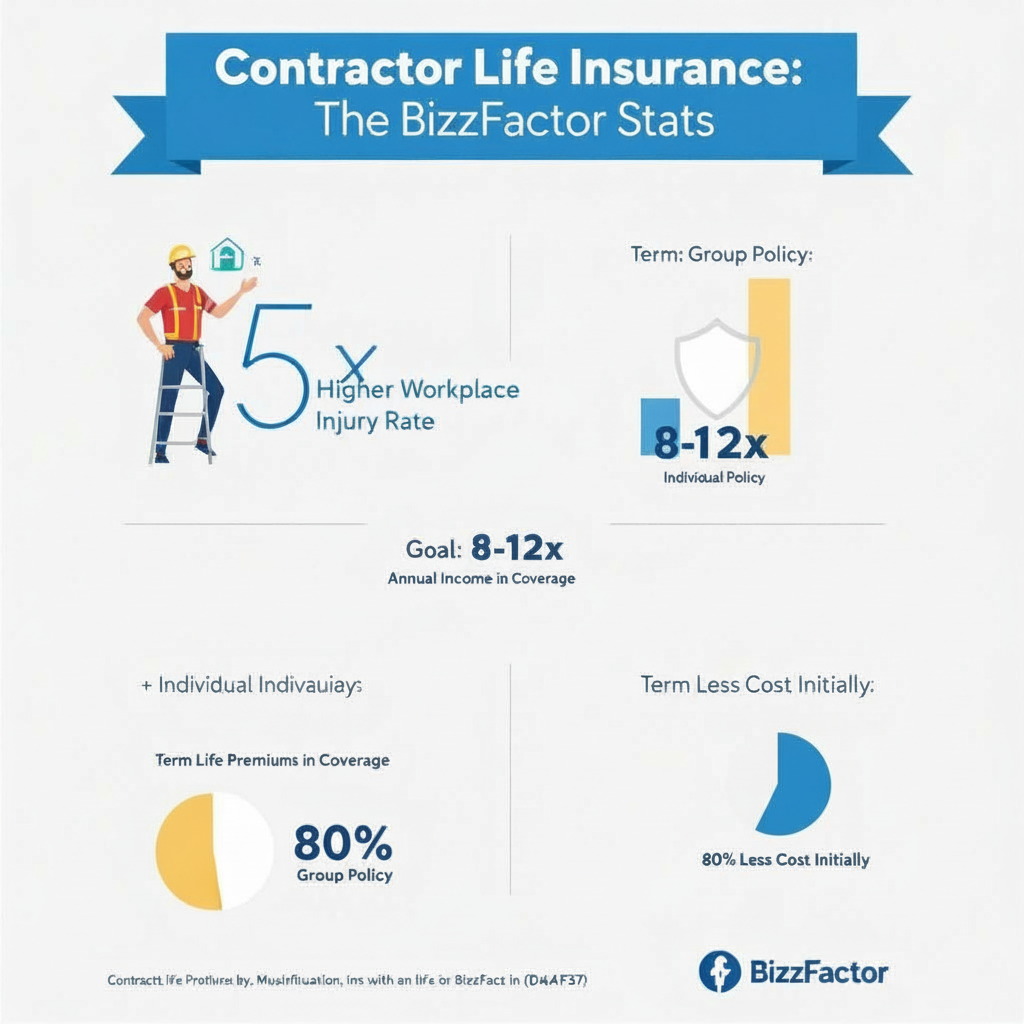

The Bureau of Labor Statistics puts workplace injuries at five times higher for contractors than desk workers. You already knew that, though — you've probably seen it happen. Maybe limped through a few close calls yourself.

Every day you're dealing with ladders, power tools, electrical panels. Heights. Heavy equipment. One slip, one distraction, one frayed wire. These risks aren't theoretical — they're Tuesday morning at 7:30 AM.

Construction has one of the highest fatality rates of any industry. Most contractors don't spend much time thinking about it (because who wants to?), but here's the reality: for most of us, we're the business. That's the real issue. Our families depend on us showing up, staying healthy, bringing home the paycheck.

One bad day changes everything.

I've watched families scramble after losing a contractor too young. Trying to keep the house. Pulling kids out of college. It's brutal, and it's avoidable.

⚠️ Critical Mistake to Avoid: Relying Solely on Trade Group Policies

Look — many contractors mistakenly believe that trade association or employer-provided group policies offer sufficient protection. A case from March 2024 really drove this home — a contractor's family received only $15,000 from their association policy. Barely covered the funeral.

Group plans? They're usually garbage:

- **Low Coverage Limits:** Frequently capping under $50,000.

- **Non-Portability:** Coverage typically terminates if you switch associations or employers.

- **Unpredictable Rates:** Premiums can increase without prior notice.

- **Lack of Control:** You have minimal say over policy terms and conditions.

An individual, private policy offers protection on *your* terms: locked-in rates, substantial death benefits, and greater flexibility.

Our BizzFactor Pro Recommendation

Instead of generic brands, focus on reputable carriers with a strong track record. BizzFactor's licensed professionals often recommend Guardian Life for contractors. They've paid dividends for over 150 consecutive years, offer robust disability riders, and their underwriters possess a nuanced understanding of trade-specific risks, including those related to roofing or specific electrical work.

What Other Advisors May Not Tell You

While "buy term and invest the difference" is a common adage, for many contractors, whole life insurance can function as a versatile financial tool. A Denver plumber we worked with in 2024 leveraged his whole life policy's cash value to finance new equipment — something impossible with term insurance. This highlights the unique advantages permanent policies can offer for business liquidity and growth.

Understanding Different Life Insurance Types for Contractors

You've got two main paths here — and honestly, most contractors need to think about both at different stages. Let's break down what actually matters (and skip the insurance-speak nobody understands).

Term Life Insurance: Maximum Coverage, Affordable Premiums

Term life gives you the biggest bang for your buck. Period.

If you're a younger contractor carrying a mortgage and raising kids, this is probably where you start. You're getting serious protection — we're talking hundreds of thousands of dollars — for what amounts to a couple of nice dinners out each month.

#### Benefits of Term Life Policies:

- **Lower Premiums:** Often 80% less expensive than comparable whole life policies.

- **High Coverage Amounts:** Available from $100,000 to over $5 million.

- **Renewable:** Many policies allow renewal without new medical exams, though at a higher rate.

- **Convertibility:** Option to convert to a permanent policy before a specified age (e.g., 65), providing long-term flexibility.

The catch? When the term ends, so does your coverage. And if you want to renew, the rates can jump significantly.

Permanent Life Options: Lifetime Coverage and Cash Value Growth

Whole life and universal life stick with you forever (assuming you keep paying). They also build cash value you can borrow against.

Think of it as insurance that doubles as a bank account you can tap when business gets tight or opportunity knocks.

**What you're actually getting:**

- Coverage that doesn't expire at 65 when you might actually need it

- Cash value growth that's tax-deferred (the IRS doesn't touch it while it's sitting there)

- Borrowing power for business expenses, equipment upgrades, whatever

- Fixed premiums with whole life, flexible payments with universal

Yeah, they cost way more upfront than term. An electrician in Sandy Springs pays $320/month for his whole life versus $65 for term. But he's buying something completely different — protection that lasts his entire life plus a growing asset he can use while he's alive.

Real Contractor Success Story: Securing Family and Business Future

October 2024, we're working with this 35-year-old HVAC guy in Denver. Business is absolutely exploding — he'd gotten a killer lead from HomeAdvisor, trucks are booked solid, he's hiring.

Then his wife asks him about life insurance.

Turns out his employer policy? Fifty grand. That's it.

They sat down and really looked at what his family would need if something happened:

- **Mortgage:** Still owed $280,000 on the house

- **Income replacement:** He was pulling about $65K/year, figure 10 years minimum — that's $650,000

- **Kids' college:** Two kids (8 and 12), probably $100K each at least

- **Funeral and immediate expenses:** Another $20,000

You do the math — they needed over a million dollars in coverage, and he had fifty grand.

First step was a $1 million, 20-year term policy. Seventy-eight bucks a month. Done. Family protected.

Six months later, business is still growing. He's expanding into residential install work, meeting all the IBC requirements, looking really solid. That's when we added a $250,000 whole life policy — something permanent he could borrow against, build cash value. Seriously. Smart move for someone with a growing business who might need capital down the road.

How Much Life Insurance Do Contractors Truly Need?

Here's the thing: most contractors need somewhere between 8-12 times their annual income in coverage. This isn't some arbitrary number — it accounts for immediate debts, income replacement for dependents, and future expenses. Way more accurate than those generic online calculators.

Step-by-Step Coverage Calculation:

**Income Replacement First**

Grab your tax return. What'd you actually make last year? Now multiply that by somewhere between 8 and 10. That's the money your family needs to have breathing room — time to grieve, figure out next moves, maybe retrain for a different career without panic selling the house.

**Add Up What You Owe**

Everything. Right now. Be honest:

- What's left on the mortgage?

- Business loans — all of them

- That equipment you're financing

- Credit cards, personal loans, the whole mess

Write it down and add it up.

**Future Stuff You Can't Ignore**

Now, now the harder part:

- College is running $35,000+ per kid per year in 2024. Multiply by however many kids you've got.

- If your spouse needs to go back to school or get certifications to work full-time, that costs money

- Childcare while they're working — that's not cheap either

**Your Business Complications**

This is where contractors get tripped up:

- Did you personally guarantee any business loans? (Most of us did.)

- Got a partner? What happens to your share of the business?

- Are you the key person keeping clients happy and checks coming in?

**Here's What It Looks Like**

Say you're making $65,000 a year. Ten times that's $650,000 just for income replacement. You've still got $200,000 on your mortgage. College fund for two kids, figure $70,000 at minimum (and that's being optimistic).

You're already at $920,000.

Rounding to a million? Yeah, probably makes sense.

Industry-Specific Contractor Considerations: Underwriting and Premiums

So — here's where it gets weird. Insurance underwriters see "contractor" on your application and immediately start doing math that has nothing to do with your actual health. They want to know if you're the general contractor standing on the ground with a clipboard or the roofer doing tear-offs in July.

Huge difference.

I've watched two 40-year-old guys — same weight, same blood pressure, both non-smokers — get quoted $180 versus $420 per month for identical coverage. Only difference? One was a finish carpenter, the other installed cell towers.

(This is why working with someone who actually understands trade classifications matters. BizzFactor's team works exclusively with carriers who get the difference between residential electrician work and high-voltage industrial jobs.)

Risk Classifications Explained

They've basically got you in buckets before you finish the application:

**Low-Risk Contractors** (think general contractor doing light commercial, mostly supervisory)

- You're getting standard or even preferred rates

- Pretty much any rider you want is available

- Multiple carriers will compete for your business

**Medium-Risk Trades** (HVAC techs, residential plumbers, inside electricians)

- Rates run maybe 15-30% higher than office workers

- Most riders available, occasional restrictions

- Solid carrier options, some shopping required

**High-Risk Specialists** (roofers, tower climbers, hazmat handlers)

- Premiums can double or triple

- Limited rider availability, strict underwriting

- Fewer carriers willing to write policies

Which category you land in affects everything — your monthly payment, what add-ons you can get, even whether certain insurance companies will talk to you at all.

Factors Influencing Your Premiums

What underwriters actually dig into during the process:

- How often you're working above 15 feet (daily height exposure is a big flag)

- What kind of power tools you're running and how frequently

- Your safety record over the past 3-5 years — any workers' comp claims?

- Whether you're OSHA compliant (they actually verify this)

- Specific trade certifications you hold

Look — real talk — we've seen premium differences up to 200% between carriers for the exact same contractor. Same age, same health, same job. One company sees "roofer" and thinks worst-case scenario, another specializes in construction trades and prices you fairly.

Shopping around isn't optional. It's mandatory.

Group vs. Individual Life Insurance: The Real Truth for Contractors

Group policies feel convenient. Sign a form at the trade association meeting, done, check the box, you're "covered." Except you're probably not — at least not enough to actually protect your family.

Here's what most group policies actually give you:

Why Group Policies Typically Fall Short

- **Coverage caps out pathetically low:** Usually 1-2x your salary, rarely over $100,000. You read that mortgage calculation section above? This doesn't even come close.

- **It vanishes when you leave:** Switch employers, drop the association membership, start your own shop? Coverage gone.

- **You can't control who gets the money:** Way less flexibility on beneficiaries than you'd think.

- **Zero cash value:** It's not building anything. Pure expense.

An electrician in Marietta told me last year, "I figured I was set with my union policy. Then I actually read it — $40,000. That wouldn't even pay off my work truck."

Advantages of an Individual Life Insurance Policy

When you own your own policy:

- **You decide the coverage amount:** Need $1.5 million? Done. Want $500K? Also fine. It's your call based on your family's actual needs.

- **It's YOURS:** Change jobs seventeen times, doesn't matter. Start your own business, retire, move to Florida — policy stays with you.

- **Way more options:** Term, whole life, universal life, guaranteed issue, whatever fits your situation and budget.

- **You control everything:** Beneficiaries, riders, how it pays out, all of it.

Group policies are fine as a bonus. Free money, take it. But relying on them as your primary protection? That's gambling with your family's future.

In-Depth Look

Detailed illustration of key concepts

Visual Guide

Infographic illustration for this topic

Side-by-Side Comparison

Visual comparison of options and alternatives

Sources & References

- Your Guide to Home Insurance in 2024: Top 7 Trends & Strategies

- Guide For Contractors Insurance and Handyman Insurance

- Contractor Insurance is Essential for Home Improvements

- Your Essential Guide to Homeowners Insurance in 2024

- A Guide To Contractor Insurance in 2024 - LandesBlosch

- Building Codes, Standards, and Regulations: Frequently Asked ...

- Building Codes and Standards - 101 Guide | ROCKWOOL Blog

- [PDF] Building Codes Toolkit for Homeowners and Occupants - FEMA

- Amazon Best Sellers: Best Architectural Codes & Standards

- ICC - International Code Council - ICC

Frequently Asked Questions

Need Professional Help?

Find top-rated insurance services experts in your area