Calculate life insurance for stay-at-home parents with our licensed team. We value $180K+ in contributions and find proper coverage to protect your family.

Key Takeaways

Life Insurance for Stay-at-Home Parents: Comprehensive Coverage Guide for 2024

Stay-at-home parents (SAHPs) are the unsung heroes of countless households, orchestrating a complex symphony of tasks that range from nurturing and educating children to meticulously managing household affairs, preparing nourishing meals, and coordinating intricate family schedules. This extensive, often invisible and unpaid, labor generates immense economic value that is frequently overlooked or underestimated in conventional financial planning and life insurance discussions. Traditionally, when families consider life insurance, the primary focus tends to gravitate towards the income-earning parent. However, this narrow perspective can lead to a significant and potentially catastrophic financial gap if the invaluable contributions of a stay-at-home parent are not adequately insured. This comprehensive guide delves into the critical importance of life insurance for stay-at-home parents, illuminating its multifaceted role in safeguarding a family's financial future and providing practical methodologies for calculating appropriate coverage in 2024.

The Indispensable Economic Value of Stay-at-Home Parents: Quantifying Unpaid Labor

The contributions of a stay-at-home parent are far-reaching and encompass a vast array of essential services. If these services were outsourced to professionals, they would inevitably incur substantial costs, placing immense strain on a family's budget. The economic roles fulfilled by a SAHP are diverse and critical, operating 24/7 without a traditional salary:

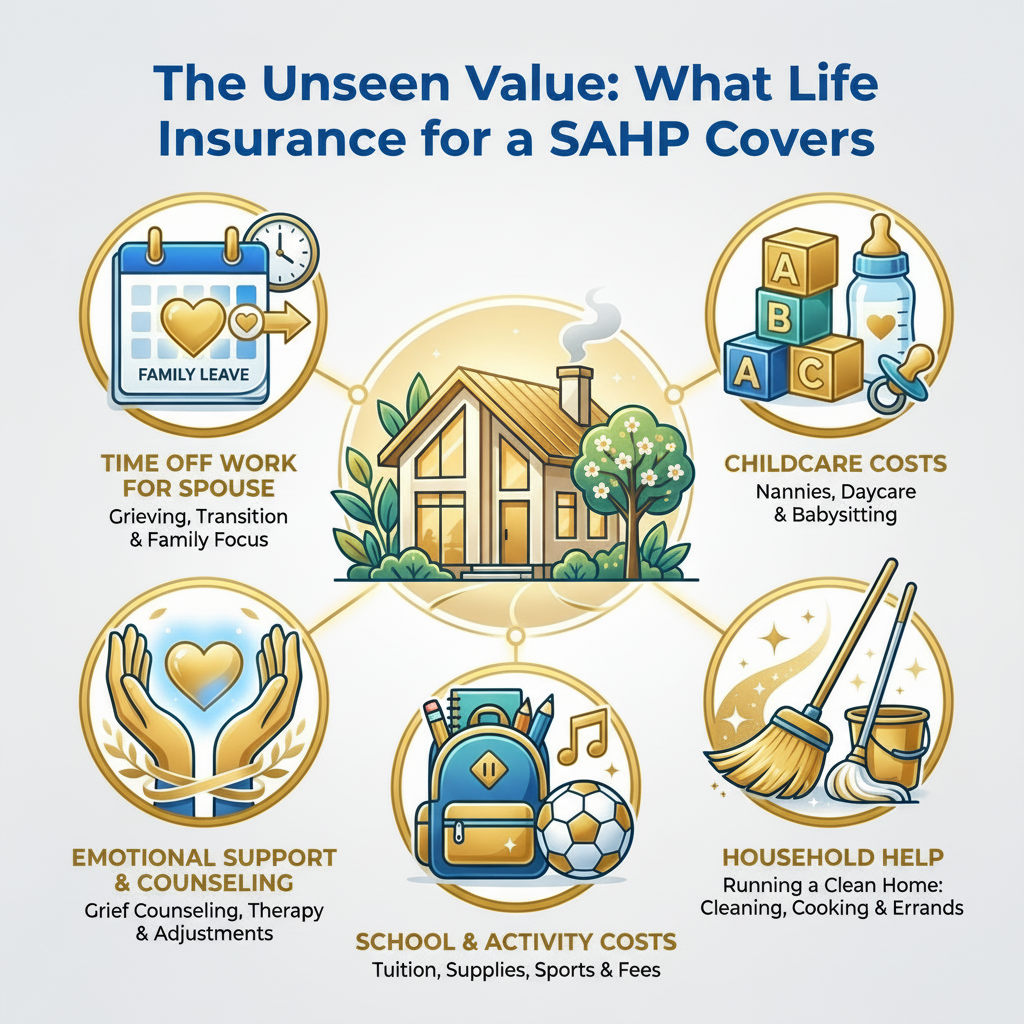

- **Childcare Provider:** This pivotal role involves nurturing, educating, supervising, and entertaining children, adapting to various developmental stages from infancy through adolescence. Professional childcare costs, particularly for infants or multiple children, can easily exceed an annual salary in many regions. According to Child Care Aware of America's 2023 data, the average cost of infant care ranges from \$9,000 to over \$20,000 annually, depending on the state and facility type. For a live-in nanny, annual costs can reach \$40,000 to \$70,000+, excluding room and board.

- **Household Manager/Administrator:** Responsible for coordinating family schedules, managing appointments (medical, dental, extracurricular), planning vacations, overseeing household projects, and maintaining family logistics. This function is akin to a project manager or personal assistant, demanding significant organizational and logistical expertise. A professional personal assistant can charge \$20-50 per hour.

- **Chef/Nutritionist:** Planning balanced meals, grocery shopping, meal preparation, and often catering to specific dietary needs or restrictions. The average cost of a private chef or regular meal delivery service for a family is substantial, easily running into hundreds or thousands of dollars monthly. Custom meal prep services for a family can cost upwards of \$15,000 annually.

- **Cleaner/Housekeeper:** Maintaining a clean, organized, and hygienic living environment, including regular cleaning, laundry, and decluttering. Professional cleaning services, even on a weekly basis, represent a significant expenditure, often \$150-\$300 per visit, totaling \$7,800-\$$15,600 annually for weekly service.

- **Financial Manager/Bookkeeper:** Budgeting, bill paying, managing household accounts, shopping for household necessities, and contributing to long-term financial planning. This role often involves detailed tracking and optimization of household expenses, potentially saving the family thousands annually through prudent management and strategic purchasing.

- **Personal Assistant/Errand Runner:** Handling daily errands, transportation to school and activities, managing repairs, and often acting as the primary point of contact for external services and family needs. This saves the working parent valuable time and allows them to focus on their professional responsibilities, contributing indirectly to the family's income.

- **Educator/Tutor:** Assisting with homework, teaching foundational skills, and supporting intellectual development, particularly for younger children. Private tutoring can be quite expensive, ranging from \$40-\$$100+ per hour, even for a few hours a week. For a child needing consistent support, this can easily amount to \$5,000-\$10,000+ per year.

- **Counselor/Psychological Support:** Providing emotional support, conflict resolution, and guidance for children and other family members. While not a professional therapist, the emotional labor and support provided are invaluable for family well-being, fostering a stable home environment.

- **Nurse/Health Coordinator:** Administering basic first aid, coordinating doctor's appointments, managing medications, and ensuring the family's general health and well-being. This can involve significant time and advocacy, especially if a family member has chronic health needs or requires frequent medical attention. Hospital stays or long-term care for family members would escalate this role significantly.

Quantifying the Economic Contribution: Data and Statistics

Individually, each of these services commands a market rate, often a high one. Collectively, they represent a monumental economic contribution that, if suddenly lost due to the death of a stay-at-home parent, would necessitate expensive and immediate replacement. Effective life insurance planning must rigorously reflect these "replacement costs" to ensure the surviving family's sustained financial stability and quality of life.

- **Salary.com's annual Mom Salary Survey:** In 2023, this widely cited survey estimated the median annual 'salary' of a stay-at-home parent, if their services were paid for at market rates, to be over \$180,000. This calculation considers the market rates for roles like CEO (household management), nutritionist, psychologist, facilities manager, and more, based on a 96.6-hour work week. This figure is a conservative estimate, as it doesn't always account for regional variations or specialized needs.

- **Bureau of Labor Statistics (BLS):** While not directly calculating SAHP salaries, BLS data on occupations relevant to SAHP roles (e.g., childcare workers average ~\$30,000/year, housekeepers ~\$35,000/year, personal care aides ~\$32,000/year) provides a foundational method for estimating replacement costs for individual services. The cumulative effect multiplies these figures, showing a multi-faceted salary equivalent.

- **Child Care Aware of America:** Reports that childcare is one of the largest expenses for families, often exceeding housing costs in many states. The average annual cost for an infant in a center can range from \$9,000 to over \$20,000, depending on the state, significantly impacting family budgets and highlighting a major replacement cost.

- **Council For Disability Awareness:** Highlights the financial vulnerability of families when a non-wage earner is lost or disabled, stressing the need for comprehensive protection beyond just income replacement for the primary earner. They emphasize that the economic impact extends beyond direct income.

These figures underscore the significant financial void left by the absence of a SAHP and highlight the necessity of substantial life insurance coverage. The economic output of a stay-at-home parent, although unpaid, is a critical component of household stability and prosperity, acting as a foundational support structure for the family's overall well-being.

The Profound Impact of a Stay-at-Home Parent's Loss: Beyond Emotional Grief

The loss of a stay-at-home parent is emotionally devastating, but its repercussions extend far beyond psychological grief. It creates immediate and pervasive financial burdens for the surviving spouse and children, drastically altering their daily lives. The working parent would abruptly be confronted with a cascade of new responsibilities and associated costs, often with little to no financial preparation:

- **Immediate & Long-Term Childcare Expenses:** This is often the most substantial and critically urgent cost. It could involve full-time daycare, hiring a live-in or live-out nanny, enlisting au pairs, or enrolling children in expensive after-school programs and summer camps. For infants and toddlers, these costs can easily reach \$15,000-\$$30,000+ annually per child in many urban areas. According to Child Care Aware of America's 2023 report, childcare costs surpassed housing costs in 35 states for single parents, highlighting the economic strain. A live-in nanny, for instance, can cost \$40,000-\$$70,000+ per year, plus room and board, becoming an immediate and profound financial strain.

- **Household Support Services:** Hiring professionals for cleaning, laundry, regular meal preparation or a personal chef, and general home maintenance. This could cost thousands annually, depending on the frequency and scope of services. A weekly cleaning service and bi-weekly meal prep could easily exceed \$15,000 annually. The absence of a SAHP also means increased deferred maintenance if these services aren't replaced, leading to larger costs down the line.

- **Educational and Extracurricular Activity Costs:** This includes paying for private transportation to and from school, after-school clubs, sports activities, art classes, and potentially private tutoring to support academic performance. The logistical coordination alone is a major undertaking, and hiring a personal assistant for such tasks could be an additional \$20-50 per hour, adding up to thousands annually, vital for children's development and mental health.

- **Therapeutic and Emotional Support:** Potential costs for grief counseling or psychological therapy for the surviving parent and children to navigate the profound emotional trauma and adjustment to life without the SAHP. These services can be vital for long-term emotional well-being and can range from \$100-\$$250+ per session, and often required for extended periods, representing a significant cumulative cost.

- **Lost Work Productivity and Career Impact:** The surviving parent may be forced to reduce their work hours, decline promotions that require more time, take extended leaves of absence (paid or unpaid), or even completely leave the workforce to manage newfound domestic and childcare responsibilities. This directly impacts their current income, future earning potential, and career progression, leading to a significant decrease in household income. A study by the Center for American Progress found that parents who take time off work or reduce hours for caregiving can lose hundreds of thousands of dollars in lifetime earnings, severely impacting retirement security.

- **Reduced Quality of Life:** The cumulative effect of these financial and logistical stresses can lead to a substantial reduction in the family's overall quality of life, necessitating sacrifices in areas like housing, education, and leisure activities. The emotional toll, often underestimated, can also lead to health issues for the surviving family members due to chronic stress, further escalating costs (e.g. medical bills) and decreasing productivity.

These costs are not fleeting; they evolve and often persist for many years, adapting to the children's changing ages and developmental needs. This demands a robust and sustained financial plan, precisely what life insurance for a stay-at-home parent aims to provide. Without adequate coverage, the family system can destabilize financially and emotionally, leading to long-term hardship.

Tailoring Life Insurance Coverage: A Precise Calculation for 2024

Determining the appropriate life insurance amount for a stay-at-home parent necessitates a meticulous evaluation of potential replacement costs and a forward-looking assessment of the family's future financial landscape. While the precise amount varies, many financial experts advocate that stay-at-home parents should carry coverage comparable to or even exceeding that of working parents, carefully adapted to their specific household dynamics and future needs.

Key Considerations for Robust Coverage Planning in 2024:

1. **Age and Number of Children:** This is paramount. Younger children, especially infants and toddlers, generally require more intensive, round-the-clock, and costly care. A family with multiple young children will face exponentially higher replacement costs than one with older, more independent children. The duration of care needed is a primary factor. A 2-year-old child will require approximately 16 years of care until adulthood, while a teenager might need only a few.

2. **Current & Projected Cost of Childcare:** Research the prevailing market rates for nannies, au pairs, daycare centers, and after-school programs in your specific geographic area. Factor in potential inflation over the years. This can arguably be the largest component of the calculation. Utilize local childcare resource agencies, such as those governed by the *National Association of Child Care Resource & Referral Agencies (NACCRRA)*, for accurate, localized data and quality standards. Consider the *Child Care and Development Block Grant (CCDBG) Act of 2014* which sets health and safety standards for child care providers.

3. **Cost of Household Management & Services:** Estimate the annual expenses for hiring professional cleaners, a meal delivery service or part-time cook, a personal assistant for errands, and general home maintenance. Consider what level of service would be needed to maintain the current household standard for duration consistent with the family's need (e.g., until children are independent or until the surviving spouse retires). Engage with reputable service providers and obtain quotes to ensure realistic budget projections.

4. **Family Debt Obligations:** Include outstanding balances on the mortgage, car loans, student loans, personal loans, and credit card debts. The life insurance payout should ideally provide enough to pay off or significantly reduce these debts, alleviating a major financial burden for the surviving spouse and increasing financial liquidity. This debt elimination can free up significant monthly cash flow, enabling the surviving parent to manage other emergent costs without additional stress.

5. **Future Educational Needs:** Account for potential college savings goals for the children. While 529 plans and other savings vehicles are crucial, life insurance can serve as a valuable supplement or primary funding source if other means are depleted or unavailable, ensuring educational continuity and opportunity for the children. The *College Board* publishes average college costs annually, which should be factored in, anticipating inflation.

6. **Family Lifestyle Maintenance:** Ensure the payout is sufficient to allow the surviving family to maintain its current standard of living, avoiding drastic sacrifices in housing, nutrition, education, and leisure activities. This includes maintaining existing social and recreational activities for children, which contribute significantly to their well-being and stability during a traumatic period.

7. **Surviving Parent's Earning Capacity & Career Impact:** Consider whether the working parent would need to take time off, reduce hours, or hire additional support which would impact their income. The life insurance policy should compensate for this potential income reduction and provide a buffer during a period of intense grief and adjustment, preventing a compounding financial crisis.

8. **Inflation:** Factor in a reasonable inflation rate (e.g., 2-4% per year, often exceeding current CPI for services like healthcare and education) for projected costs, especially over long policy terms. The purchasing power of money diminishes over time, so calculations must account for future cost escalation to ensure the coverage remains adequate.

9. **Final Expenses:** Include a buffer for funeral costs, memorial services, probate fees, and other end-of-life expenses, which typically range from \$10,000 to \$20,000 based on data from the *National Funeral Directors Association (NFDA)*. This ensures that a grieving family does not face immediate financial strain for these necessary arrangements.

**Example Calculation for a Family with Two Young Children (ages 2 & 5) in a Moderate Cost-of-Living Area:**

- **Childcare (16 years until youngest is 18):** Nanny/Daycare costs estimated at \$2,500/month for both children, adjusted for inflation (assume total childcare including after-school/summer camp for older child) = \$30,000/year x 16 years = \$480,000. Applying an average inflation factor over 16 years (e.g., 3%) can push this closer to \$600,000.

- **Household Services (16 years):** Cleaning (\$500/month) + Meal Prep/Errands (\$1,000/month) = \$1,500/month or \$18,000/year for 16 years = \$288,000.

- **Debt Payoff:** Remaining Mortgage = \$300,000; Car Loan = \$20,000; Student Loans = \$50,000. Total Debt = \$370,000.

- **Education Fund Contribution:** \$100,000 per child (supplementary to existing savings if needed) = \$200,000.

- **Survivor Income Support (for career impact/transition and emotional support):** \$50,000 per year for 3 years (to allow significant adjustment and career restructuring) = \$150,000.

- **Final Expenses:** \$15,000.

**Total Estimated Coverage Needed: Approximately \$600,000 (childcare) + \$288,000 (household services) + \$370,000 (debt) + \$200,000 (education) + \$150,000 (income support) + \$15,000 (final expenses) = \$1,623,000.**

This robust example demonstrates that the amount needed can easily run into seven figures. Working directly with a licensed insurance professional or a CERTIFIED FINANCIAL PLANNER™ (CFP®) is paramount to accurately assess these unique needs and calculate a precise, suitable coverage amount, going far beyond the limitations of generic online calculators. They can help navigate complex scenarios, offer tailored recommendations, and ensure compliance with various state insurance regulations. Industry standards from organizations like the *National Association of Insurance Commissioners (NAIC)* guide ethical practices and consumer protection.

Structuring Life Insurance Policies for Maximum Flexibility and Value

Families have a broad spectrum of options when structuring life insurance to align with their unique needs, financial goals, and budgetary constraints. A well-designed policy structure can provide both immediate protection and long-term financial stability.

Combining Term and Permanent Policies: A Hybrid Strategy

A highly recommended and increasingly common strategy involves integrating both term and permanent life insurance components to optimize coverage and cost-effectiveness, providing layered protection:

- **Term Life Insurance:** This type of policy provides coverage for a specific, predetermined period, typically 10, 20, or 30 years. It is particularly well-suited for covering periods of peak financial responsibility, such as the years when children are young, the mortgage is substantial, or significant debts are outstanding. Term life is generally more affordable than permanent life insurance, allowing for substantial coverage for a limited duration. It functions purely as an income replacement and debt coverage tool, offering a pure death benefit. For a SAHP, a 20- or 30-year term policy would likely cover the critical child-rearing years until children achieve financial independence. Many policies are guaranteed renewable, though premiums may increase significantly after the initial term. The key advantage is high coverage at a lower initial cost.

- **Permanent Life Insurance (e.g., Whole Life, Universal Life):** This offers lifelong coverage, provided premiums are paid, and typically accumulates cash value over time on a tax-deferred basis. This cash value can be accessed later through loans or withdrawals for various purposes, such as supplemental retirement income, college expenses, or emergencies. While more expensive, a smaller permanent policy for a SAHP can cover final expenses, provide a small inheritance, or offer long-term financial security beyond the immediate needs of a term policy. Some types, like Guaranteed Universal Life (GUL), offer lifelong coverage at a lower cost than Whole Life, but with less emphasis on cash value growth. Variable Universal Life (VUL) offers investment options but carries market risk. These policies are often chosen for estate planning or wealth transfer.

The optimal structure strategically balances immediate budget constraints with comprehensive, enduring protection. For many SAHPs, a significant term policy to cover the years of highest dependency, potentially coupled with a smaller permanent policy for lifelong needs, offers an excellent compromise, providing robust safety and flexibility. This dual approach ensures both immediate protection during critical phases and sustained security for the long haul.

Adaptable Policy Options and Advanced Riders: Enhancing Coverage Fidelity

Look for policies that incorporate flexibility, allowing for adjustments as life circumstances inevitably change. Significant life events—such as paying off a mortgage, children achieving financial independence, a surviving spouse remarrying, or substantial shifts in household income—might necessitate modifications to your policy. Riders are contractual provisions added to a basic policy that enhance or modify its coverage, often for an additional premium. Each rider has specific conditions and benefits regulated by state insurance departments.

#### Essential Policy Features and Riders to Consider for SAHPs:

- **Guaranteed Insurability Rider (GIR):** This invaluable rider allows the policyholder to purchase additional coverage at specific future intervals (e.g., after the birth of a child, marriage, home purchase, or every few years on key policy anniversaries) without undergoing a new medical examination or proving insurability. This is crucial for career progression or expanding families, ensuring you can increase coverage even if your health declines, complying with *NAIC Model Regulation #270* which provides guidelines for the content and disclosure of such riders. This is especially useful as a SAHP's 'economic value' grows with more children or increased responsibilities.

- **Accelerated Death Benefit (ADB) Rider / Living Benefits Rider:** This allows early access to a portion of the death benefit (typically 25-90%, up to a certain financial cap set by the insurer, e.g., \$250,000) if the insured is diagnosed with a terminal or critical illness with a life expectancy typically of 12-24 months. The funds can be used to cover medical expenses, home modifications, or end-of-life care, providing financial relief during extremely challenging times. Specific state regulations (e.g., through the *Department of Insurance*) dictate the maximum benefit and qualifying conditions, ensuring consumer protection.

- **Waiver of Premium Rider:** This critical rider waives future premium payments if the insured becomes totally and permanently disabled and unable to work, as defined by the policy (usually inability to perform *any* gainful occupation). It ensures that the life insurance coverage remains active and in force during a period when income may be severely impacted, preventing policy lapse when the family is most vulnerable. This rider often has a waiting period (e.g., 90 days or 6 months) before benefits begin, and requires specific medical documentation.

- **Child Rider:** Provides a small amount of often convertible term life insurance coverage (e.g., \$5,000-\$$25,000) for each child, often convertible to a permanent policy later in the child's life without requiring new medical underwriting. This can cover final expenses for a child (a tragic but real need) or provide a valuable future insurability option for them at adulthood, allowing them to secure their own coverage regardless of future health conditions.

- **Return of Premium (ROP) Rider (for Term Policies):** If the policyholder outlives the term of the policy, this rider refunds all premiums paid. While it makes premiums significantly higher (sometimes 50-100% more than a standard term policy) and often exceeds the potential earnings from investing the difference, it can appeal to those who view life insurance as an investment or who are hesitant about "wasting" premium payments on a policy that isn't utilized. It essentially functions as a forced savings plan, though usually not the most efficient.

- **Convertibility Rider:** Many term policies include this standard feature, allowing the policy to be converted into a permanent life insurance policy (e.g., Whole Life or Universal Life) at the carrier's then-current rates, without a medical exam, regardless of health status. This provides invaluable flexibility for long-term planning, particularly as health may decline with age, ensuring continued coverage beyond the initial term if lifelong needs arise.

- **Spouse Rider:** Allows a separate term life policy for a spouse to be added to the primary policy, often at a reduced administrative cost compared to two standalone policies. This streamlines management for families, simplifying premium payments and paperwork.

Thoroughly reviewing all available features, understanding the benefits of different term lengths, and selecting appropriate riders are crucial steps to ensure that the chosen policy not only truly addresses the family's specific situation but also offers robust and adaptable financial protection in the face of the unexpected. An expert insurance agent can provide a *policy illustration* detailing costs and benefits over time.

The Multiple Policy Approach: "Laddering" for Optimized Value and Precision

Instead of relying on a single, monolithic policy, some financially savvy families opt for a strategy known as "laddering," which involves acquiring multiple smaller term policies with varying term lengths. This approach provides several advantages, offering superior precision and cost management, becoming a cornerstone of modern, efficient life insurance planning:

- **Optimized Coverage:** Provides higher total coverage during years of maximum financial dependency (e.g., when children are very young, and the mortgage is highest) and allows coverage to decrease naturally and cost-effectively as needs dissipate over time. For example, a family might buy a 30-year term policy for mortgage protection, a 20-year term for peak childcare costs, and a 10-year term to cover specific short-term debts. The decreasing segments align perfectly with decreasing financial burdens, rather than having uniform coverage for a long period when needs change.

- **Cost Efficiency:** Laddering can be significantly more cost-effective than taking out one large, long-term policy. As shorter-term policies expire and needs decrease, premium costs are reduced more quickly. A single 30-year term policy for \$1.5 million will be substantially more expensive over its duration than a combination of a 30-year \$500k, a 20-year \$500k, and a 10-year \$500k, especially as the shorter terms expire and premiums cease.

- **Flexibility:** Allows for more granular adjustment to changing family needs. If one critical need (e.g., specific debt is paid off early, or children become independent sooner than anticipated), that specific policy segment can be allowed to expire without impacting others. This avoids over-insuring and unnecessary premium payments, providing dynamic financial management capabilities. It also allows for easier future adjustments if new financial obligations arise.

This nuanced approach requires careful planning and coordination with a financial professional but can yield substantial long-term savings and more precisely match coverage to evolving financial obligations, aligning with best practices in risk management and personal finance. It reflects a proactive, rather than reactive, approach to family financial security.

The Application Process: Navigating Underwriting and Premiums for SAHPs

Applying for life insurance involves several steps, and understanding them can streamline the process for stay-at-home parents and significantly increase the likelihood of securing better rates and appropriate coverage.

The Underwriting Process: A Holistic Risk Assessment

Life insurance companies assess risk through a comprehensive underwriting process, which is designed to evaluate an applicant's potential mortality risk. This typically includes:

- **Application Form:** Detailed questions about personal health history (e.g., diagnoses, treatments, surgeries), family medical history (e.g., incidence of heart disease, cancer, diabetes in immediate family members), lifestyle (smoking, alcohol consumption, dangerous hobbies such as skydiving, scuba diving, aviation, motor racing), occupational details (less relevant for SAHPs, but still required), and past and current medical conditions. Honesty is crucial; any material misrepresentation can lead to policy voidance or claims denial, as per the *NAIC Unfair Trade Practices Act*.

- **Medical Exam:** Often involves a paramedical professional visiting your home or office to take vital signs (blood pressure, pulse, respiration rate), height, weight, and collect blood (for cholesterol panels, glucose levels, liver/kidney function tests, HIV antibodies, hepatitis markers) and urine samples (for nicotine metabolites, drugs, protein, glucose). This provides objective health data that supplements self-reported information. For larger policies, an Electrocardiogram (ECG) or even a treadmill stress test may be required.

- **Medical Information Bureau (MIB) Check:** The MIB is a non-profit trade association that maintains a database of coded health information among participating insurers to prevent fraud and ensure accurate disclosures from applicants across different companies. It flags inconsistencies in health statements made on applications over the past 5-7 years.

- **Prescription History Check:** Databases like Intelliscript or Milliman provide a list of all medications prescribed to an individual over a specified period (e.g., 5-7 years), offering detailed insights into diagnosed health conditions and their management, often revealing conditions an applicant might unintentionally omit.

- **Motor Vehicle Report (MVR):** Insurers may check driving records as an indicator of risk, especially for multiple traffic violations, speeding tickets, or DUI/DWI history, which can affect insurability or premium class, as reckless driving can indicate a higher risk of accidental death.

- **Public Records Search:** Verification of address, basic criminal history (felonies), and bankruptcies may also be part of the background check, as these can be indicators of moral hazard or financial instability.

Premiums are primarily determined by age, gender, health class (assigned after thorough underwriting, e.g., Preferred Best, Preferred, Standard Plus, Standard, Substandard), type of policy, and coverage amount. Healthier individuals in preferred health classes receive significantly lower rates due to their lower actuarial risk. It's crucial for SAHPs to prioritize their health, as even minor health improvements (e.g., quitting smoking, controlling blood pressure and cholesterol through diet/exercise) can lead to significantly better rates, saving thousands over the life of a policy.

Factors Influencing Premiums for Stay-at-Home Parents

While SAHPs do not have an occupational risk in the traditional sense, their premiums are still affected by several personal and policy-related factors, similar to income earners:

- **Age:** Younger applicants generally pay lower premiums because they have a longer life expectancy, making them a lower mortality risk for the insurer. Premiums typically increase with each birthday.

- **Health:** Excellent current health, a clean medical history, and well-managed existing conditions lead to preferred rates. Conditions like Type 2 diabetes, uncontrolled high blood pressure, elevated cholesterol, history of cancer, or obesity will increase premiums, often by being categorized into a substandard rating class.

- **Lifestyle:** Smoking, excessive alcohol consumption (e.g., more than 14 drinks/week for men, 7 for women), recreational drug use, and participation in dangerous hobbies (e.g., rock climbing, private piloting without proper certification, uncertified scuba diving, base jumping) significantly elevate rates due to increased risk of premature death or serious injury.

- **Policy Type and Term:** Term policies are less expensive than permanent ones per dollar of coverage due to their temporary nature. Longer term lengths for term policies (e.g., 30 years vs. 10 years) also cost more due to the extended period of risk that the insurer is obligated to cover. Permanent policy costs are higher due to the cash value component and lifelong coverage guarantee.

- **Coverage Amount:** Higher death benefits naturally lead to higher premiums. The insurer is taking on a greater financial liability, requiring a higher premium to offset that risk.

- **Insurance Carrier:** Different insurance companies have varying underwriting guidelines, risk appetites, and pricing structures based on their internal mortality tables and financial models. Therefore, comparing quotes from multiple reputable insurers is essential to find the best rate for your specific health profile. An independent agent or broker can shop the market efficiently for you.

It's important to be completely honest during the application process, as misrepresentation can lead to policy rescission (cancellation) or denial of claims, leaving your family unprotected when they need it most. Insurers operate under a "duty of good faith and fair dealing" (as outlined in contract law), and they expect the same from applicants. Transparency ensures claims are paid expeditiously.

Expert Insights and Best Practices for SAHP Life Insurance

The "Human Life Value" vs. "Needs-Based" Approach: A SAHP Focus

Traditional life insurance calculations for wage-earners often use the "Human Life Value" approach, which estimates the present value of future earnings. For SAHPs, this method is largely inapplicable given their non-wage earning status directly. Therefore, a more appropriate and widely accepted method is the "Needs-Based" approach, which focuses specifically on the financial obligations and services that would need replacement upon their death. This includes immediate expenses, ongoing living costs for the family, childcare services, education funding, debt repayment, and achievement of future financial goals. Consulting with a financial planner specializing in family financial security and life insurance is crucial to accurately apply this comprehensive approach.

Regular Policy Review and Adjustment: Dynamic Financial Planning

Life insurance needs are not static; they are dynamic and evolve significantly over time. Major life events—such as the birth of a new child, purchasing a larger home, significant career changes for the working spouse, children entering school, children leaving home, or paying off substantial debt—should trigger an immediate review of your policy. It's recommended to review your coverage at least every 3-5 years, or immediately following any significant life change, to ensure it remains aligned with your family's evolving financial landscape and needs. An under-insured SAHP policy can be almost as detrimental as no policy at all during a crisis, as it provides a false sense of security. Over-insuring can also lead to unnecessary premium costs, so striking the right balance is key.

Consider Disability Insurance for SAHPs: A Complementary Protection

While this guide focuses on life insurance for mortality risk, it's worth noting that if a stay-at-home parent becomes disabled and unable to perform their duties, the financial impact can be similar to, or even greater than, their death, due to ongoing care costs and potential need for rehabilitation. Disability insurance *for the stay-at-home parent* (often called "homemaker disability insurance" or "caregiver disability insurance") can provide a tax-free monthly benefit to cover external services like childcare, professional housekeeping, and domestic help. This safeguards the family's financial well-being during such an event by ensuring continuity of essential household services. This is a complementary, often overlooked, but vital aspect of comprehensive family financial planning, creating a layered defense against unforeseen circumstances.

Estate Planning and Legal Considerations for SAHPs

Beyond the financial payout, life insurance for a SAHP can play a crucial role in overall estate planning. Proper designation of beneficiaries is critical; ensure primary and contingent beneficiaries are clearly named and kept up-to-date, especially if trusts are involved for minor children. A will, drafted by an attorney, should also name a guardian for minor children and outline wishes for the insurance proceeds, particularly if a trust is established. The portability of policies and impact of state-specific community property laws should also be discussed with financial and legal advisors. Neglecting these legal aspects can lead to delays in payout or disbursement according to state intestacy laws, which may not align with the deceased's wishes.

Essential Steps to Take Now for Comprehensive Protection

1. **Calculate Your SAHP's Economic Value and Needs:** Utilize online calculators (with caution) and the detailed considerations outlined above to estimate the precise replacement costs of all services provided by the SAHP. Be thorough and realistic in your projections, considering the long-term compounding of costs like childcare and inflation. Don't solely rely on estimates; obtain local service quotes where possible.

2. **Determine Appropriate Coverage:** Factor in all family debts (mortgage, student loans, car loans), future goals (college, retirement for surviving spouse), and lifestyle maintenance. Aim for a figure that genuinely secures your family for a substantial period (e.g., 10-25 years) into the future, providing a sufficient safety net until children are self-sufficient and the surviving spouse has adequate time to adjust.

3. **Consult a Licensed Financial Professional:** An independent insurance agent or CERTIFIED FINANCIAL PLANNER™ can offer unbiased advice, compare quotes from multiple reputable carriers (as rates can vary by up to 30% for the same coverage cohort), and help you select the most suitable policy and riders for your unique situation. They can also explain state-specific regulations, consumer protections (e.g., state guaranty associations), and policy specifics. Look for professionals with designations such as CLU (Chartered Life Underwriter) or ChFC (Chartered Financial Consultant).

4. **Review Existing Coverage:** If you already have life insurance, ensure it's up-to-date and adequately covers both income-earning and stay-at-home parents. Many families find their coverage to be severely insufficient upon re-evaluation, especially if they haven't reviewed it in years. Update beneficiaries regularly, particularly after major life events.

5. **Prioritize Health and Wellness:** Engaging in healthy habits (e.g., regular exercise, balanced diet, avoiding tobacco) can significantly impact premium costs. Even small improvements in health metrics can drop you into a better underwriting class, saving thousands over the life of a policy. Schedule and attend regular check-ups with your physician to monitor and manage health proactively.

6. **Budget for Premiums:** Incorporate life insurance premiums into your household budget, recognizing it as a critical, non-negotiable investment in your family's future financial resilience, not merely an expense. Compare it to other essential utilities or long-term savings goals and understand its immense value.

7. **Organize and Communicate Important Documents:** Ensure all policy documents, beneficiary designations, agent contact information, and relevant financial information are stored securely (e.g., in a fireproof safe or secure digital vault) and readily accessible to your spouse or a trusted family member. It is equally important to communicate the existence and location of these documents and policies to key individuals, ensuring they know what steps to take should the unthinkable occur.

Investing in life insurance for a stay-at-home parent is not merely a financial transaction; it is a profound declaration of love, foresight, and responsibility, ensuring that your family's future, regardless of unforeseen circumstances, remains secure and stable. It transforms the abstract value of their daily dedication into a tangible financial safety net, providing peace of mind and preserving the family's quality of life for years to come.

*This guide is intended for informational purposes only and does not constitute financial, legal, or insurance advice. Always consult with a qualified financial professional, insurance agent, or attorney to discuss your specific needs and local regulatory requirements before making any financial decisions.*

", "faqs": [ { "question": "Why is life insurance essential for stay-at-home parents?",

"answer": "Stay-at-home parents provide indispensable services such as childcare, household management, meal preparation, and personal assistance, which collectively carry significant economic value. Should they pass away, the surviving spouse would face substantial costs to replace these services, along with increased domestic responsibilities. Life insurance provides the necessary financial capital to cover these replacement costs, mitigate debt, fund future expenses like college, and ensure the family's continued financial stability, preventing severe lifestyle disruptions and economic hardship. It quantifies the 'economic void' they would leave."

}, { "question": "How do I calculate the appropriate life insurance amount for a stay-at-home parent?",

"answer": "Calculation involves using a 'Needs-Based' approach. Estimate the total cost to replace all services provided (childcare, housekeeping, cooking, tutoring), considering the number and age of children, existing family debts (mortgage, car loans, student loans), and future financial goals like college education. This often results in a need for \$500,000 to over \$1.5 million. Consulting a licensed insurance professional for a personalized assessment, including inflation projections, is highly recommended to ensure accuracy."

}, { "question": "What types of life insurance policies are best for stay-at-home parents?",

"answer": "Many families find a hybrid approach most effective: a substantial term life insurance policy (e.g., 20 or 30 years) to cover the peak periods of financial dependency (like young children and mortgage payoff), often combined with a smaller permanent life insurance policy (e.g., whole or universal life). Term life offers affordable, high coverage for specific durations, while permanent life provides lifelong coverage and potential cash value accumulation for final expenses or long-term financial planning. The optimal choice depends on budget, family stage, and specific financial objectives."

}, { "question": "Can I increase my stay-at-home parent's life insurance coverage later?",

"answer": "Yes, many policies offer flexibility to increase coverage. A Guaranteed Insurability Rider (GIR) specifically allows policyholders to purchase additional coverage at specific future intervals (e.g., after the birth of a child, home purchase) without requiring a new medical exam, regardless of health changes. This rider is particularly valuable for young families expecting growth or future financial obligations. It's always advisable to review policies regularly with an agent to ensure coverage remains adequate for evolving needs and to keep beneficiaries updated."

}, { "question": "Are life insurance premiums for stay-at-home parents less expensive than for income-earning parents?",

"answer": "Premiums are primarily determined by factors like age, health, policy type, and coverage amount, not solely by employment status. While a stay-at-home parent might not have an occupational hazard that raises premiums, their individual health profile (e.g., medical history, lifestyle, nicotine use) and the desired face amount of the policy significantly influence costs. Comparing quotes from multiple carriers is essential to find competitive rates tailored to their specific circumstances."

}, { "question": "What is 'laddering' life insurance and why is it beneficial for SAHPs?",

"answer": "Laddering involves purchasing multiple smaller term life insurance policies with different term lengths. This strategy allows families to have higher overall coverage during periods of peak financial responsibility (e.g., when children are young and mortgage debt is high) and then for coverage to decrease as needs diminish over time. It can be more cost-effective and flexible than a single large, long-term policy, precisely matching coverage to evolving financial obligations."

} ], "answer_boxes": [ {

"question": "What is the equivalent "salary" for a stay-at-home parent?", "answer": "In 2023, Salary.com estimated the median annual 'salary' of a stay-at-home parent, if their services were compensated at market rates, to be over \$180,000. This calculation accounts for the cumulative cost of replacing roles like childcare provider, household manager, chef, and tutor."

}, { "question": "How do families bridge the financial gap after the loss of a stay-at-home parent?",

"answer": "Life insurance provides the essential financial capital. This payout funds professional childcare, housekeeping, meal preparation, and other outsourced services. It also helps pay off debts, contribute to children's education, and allows the surviving parent time to adjust without immediate financial collapse or significant career disruption, preserving family stability."

}, { "question": "What key factors influence life insurance premiums for stay-at-home parents?",

"answer": "Premiums are determined by age, current health status, lifestyle choices (like smoking or dangerous hobbies), the type of policy (term vs. permanent), and the coverage amount. Excellent health and a younger age typically result in lower costs. Honesty during underwriting is crucial to ensure policy validity."

} ], "answer_nuggets": [ {

"topic": "Economic Impact of SAHP Loss", "text": "Life insurance for stay-at-home parents directly addresses the hidden financial risks of their absence. Without it, families face immediate and substantial costs for daycare, nannies, and household help. This unbudgeted expenditure can severely strain finances, potentially forcing the surviving parent to reduce work hours or incur significant debt, thereby eroding the family’s economic foundation."

}, { "topic": "Strategic Policy Laddering", "text": "Expert financial planning often recommends a 'laddering' strategy using multiple term life policies. This allows families to secure higher coverage during peak dependency years (e.g., young children) while systematically reducing premiums as financial obligations decrease over time. This targeted approach offers cost-effectiveness and precise alignment with evolving family needs."

}, { "topic": "Importance of Riders", "text": "Specific riders like the Guaranteed Insurability Rider or Waiver of Premium Rider are crucial for SAHP life insurance. A GIR allows future coverage increases without medical re-evaluation, adapting to family growth. The Waiver of Premium ensures coverage continues if disability prevents premium payments, providing vital protection during incredibly vulnerable periods for the family.

In-Depth Look

Detailed illustration of key concepts

Visual Guide

Infographic illustration for this topic

Side-by-Side Comparison

Visual comparison of options and alternatives

Sources & References

- Life Insurance for Stay-at-Home Parents: Coverage & Costs

- Life Insurance for Stay-at-Home Parents Valuing Unpaid... - WeCovr

- Life Insurance Should Value Stay-at-Home Parents' Unpaid Labor

- Why Stay-at-Home Parents Need Life Insurance - NerdWallet

- Life Insurance for Stay-at-home Parents: Why It's Absolutely Essential

- Building Codes, Standards, and Regulations: Frequently Asked ...

- Building Codes and Standards - 101 Guide | ROCKWOOL Blog

- [PDF] Building Codes Toolkit for Homeowners and Occupants - FEMA

- Amazon Best Sellers: Best Architectural Codes & Standards

- Building Codes and Regulations - Illinois Capital Development Board

Frequently Asked Questions

Need Professional Help?

Find top-rated insurance services experts in your area