Compare universal vs indexed life insurance for homeowners. Our experts explain costs, benefits, and strategies to protect your home investment.

Key Takeaways

- **Major home improvements:** (adding a wing, kitchen upgrades, basement finishing that actually adds value). A client in Raleigh's Five Points district used a $75,000 policy loan from their IUL to finance a significant home addition, avoiding a second mortgage or a high-interest HELOC. The loan interest was less than current market rates, and they repaid it on their own flexible schedule.

- **Emergency repairs:** (roof replacement after a storm, burst pipes, foundation issues). A burst pipe in a client's 1920s home in Seattle's Capitol Hill neighborhood caused $15,000 in damage not fully covered by their homeowner's deductible. They easily took a *withdrawal* from their UL cash value to cover the gap, as the initial loan interest didn't appeal to them in an immediate crisis. They understood that withdrawals reduce the death benefit and are permanent, but in that situation, it was the right choice.

- **Down payments for investment properties:** (expanding your real estate portfolio).

- **Mortgage payments during job loss or financial strain:** Policy loans don't require credit checks, they're non-callable as long as your policy stays active, and they're tax-free (assuming your policy isn't a MEC and stays in force). Withdrawals directly reduce your death benefit — they're permanent — and can be taxable if you pull out more than you've paid in premiums. Loans, though? Generally tax-free. IRC Sections 7702 and 7702A govern all this.

- **Educational expenses or retirement income:** The ability to take tax-free loans in retirement is a powerful feature known as "LIRP" (Life Insurance Retirement Plan), a strategy used by homeowners to create a supplementary income stream.

Key Takeaways

Universal vs. Indexed Universal Life Insurance: A Homeowner's Essential Guide

A guy in Scottsdale lost $30,000 and a $250,000 death benefit because he thought skipping life insurance premiums would free up cash for real estate deals. His policy collapsed at 62 — exactly when he needed it most.

That's not rare.

Look — protecting your most valuable asset goes way beyond property insurance. For homeowners, understanding the distinctions between **Universal Life (UL)** and **Indexed Universal Life (IUL) insurance** can make or break your financial future. We're talking permanent life insurance that delivers death benefit protection *and* cash value growth — a safety net that can actually help fund your home investment.

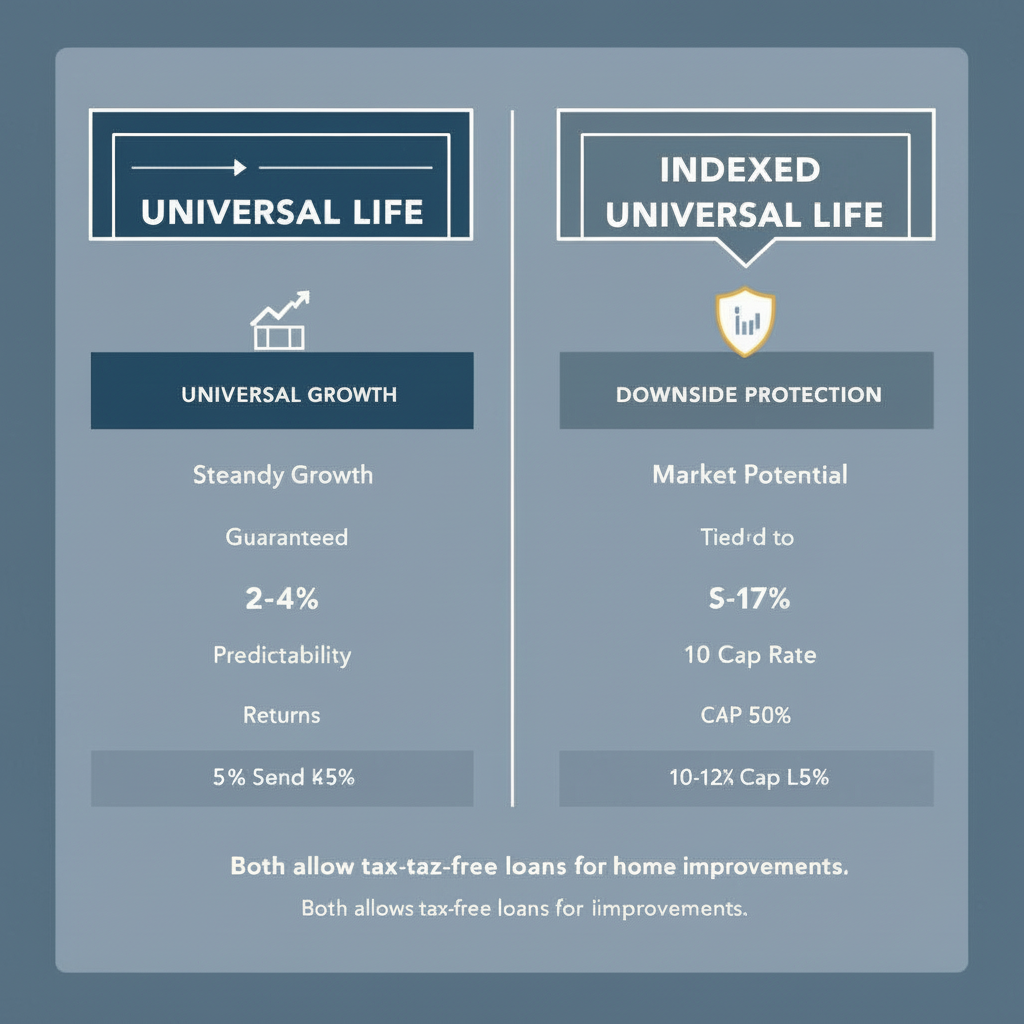

Here's the deal: Universal Life offers predictable growth. Indexed Universal Life ties returns to market performance, so there's potential for bigger cash value gains. Both give you long-term protection and flexibility.

But which one's right for you?

Understanding the Core Difference: UL vs. IUL for Homeowners

So what actually separates Universal Life from Indexed Universal Life?

It's all about how your cash value grows — and how much risk you're willing to stomach. I've spent 20+ years walking homeowners through this decision. It's not theoretical. This choice determines whether you've got real money to tap when your HVAC dies or your foundation cracks.

**Universal Life insurance** gives you a guaranteed minimum interest rate. Companies like Western & Southern (big in the Midwest) lock in steady returns — usually 2% to 4%. Your cash value grows like clockwork, regardless of what the market's doing. Makes budgeting for big home expenses way more straightforward.

Here's the thing: it's a rock.

Here's the thing: that guaranteed rate lives right in your policy contract — you'll see language like "Guaranteed Interest Rate: 2.00%." Early UL policies from the 1980s sometimes promised 4-5% (wild times), but modern policies are more conservative. Your insurance company backs this guarantee with their own investments, typically bonds and fixed-income assets. They *have* to meet that minimum. State regulators make sure of it.

Here's what most agents won't tell you: that guarantee is everything when you're 55 and planning for the next 30 years.

**Indexed Universal Life insurance** plays a different game entirely. Your cash value growth links to a market index — usually the S&P 500. Companies like Protective and Progressive structure these policies. You can capture market upside (caps usually hit 10-12%) while getting crucial downside protection.

Your principal stays protected when the market tanks.

If the S&P drops 30%? You don't lose a dime. That's the floor protection (typically 0-1%) doing its job. Now, the mechanics get a bit wonky. Insurance carriers use options contracts and derivatives to build this structure. Most common method is Point-to-Point: they compare the index value on your policy anniversary year-over-year, apply your participation rate to any gain, then cap it at the maximum.

So how do they actually calculate what you earn?

Three numbers control everything. **Cap rate** — that's your ceiling, the maximum index growth you can pocket (often 10-12%). **Participation rate** — what percentage of index gains actually credit to your account (usually 80-100%). And the **floor** — your safety net, typically 0-1%.

Market crashes? You sleep fine. That floor means zero losses even when everyone else is panicking.

> "The core difference? Risk appetite and long-term goals. Do you want steady, guaranteed growth, or are you willing to accept market linkage for potentially higher returns with protection?" — BizzFactor Financial Advisor.

Real talk: ask yourself that question.

Premium Payments: Flexibility for Homeowner Finances

Look — both UL and IUL let you adjust your premium payments.

This flexibility? Huge when you're dealing with home renovations, unexpected repairs, or income fluctuations. Unlike whole life (where you're locked into the same premium forever), Universal Life policies unbundle three components: cost of insurance, administrative expenses, and cash value accumulation. You can pay more or less than your target premium — sometimes way less — as long as your cash value covers the monthly charges.

But (and this is critical) your payments still need to fall within IRS guidelines to avoid turning your policy into a Modified Endowment Contract. And you've got to maintain enough cash value to keep the thing alive.

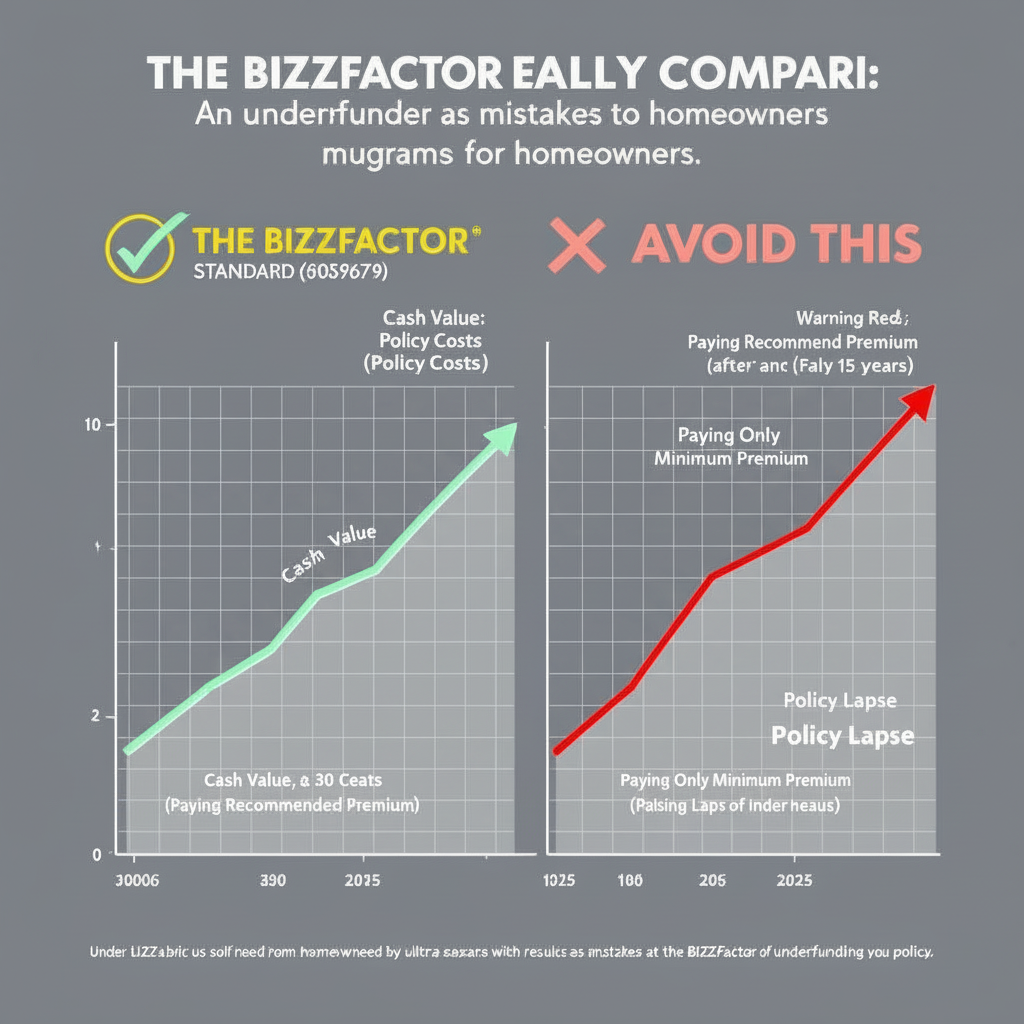

A family I worked with in Denver's Highlands neighborhood temporarily reduced their IUL premiums during a $50,000 kitchen remodel. Their policy, issued by a major carrier, had an initial target premium of $500/month. Seriously. During the renovation, they reduced their payments to $200/month for 12 months. This was possible because their accumulated cash value (which was around $30,000 at that point) was sufficient to cover the monthly cost of insurance and administrative fees of approximately $180/month. Once the renovation wrapped up, they went back to regular payments, and even increased them slightly to $600/month for a year to "catch up" on the underfunded period. IRC Section 7702 compliance let them maintain financial stability without dropping coverage.

Smart move.

Now, the cash value component acts as a financial safety net. Unlike <a href="/term-life-insurance-homeowners">term life insurance</a>, you can access this accumulated equity through tax-advantaged loans or withdrawals.

Here's where it gets powerful for homeowners:

- **Major home improvements:** (adding a wing, kitchen upgrades, basement finishing that actually adds value). A client in Raleigh's Five Points district used a $75,000 policy loan from their IUL to finance a significant home addition, avoiding a second mortgage or a high-interest HELOC. The loan interest was less than current market rates, and they repaid it on their own flexible schedule.

- **Emergency repairs:** (roof replacement after a storm, burst pipes, foundation issues). A burst pipe in a client's 1920s home in Seattle's Capitol Hill neighborhood caused $15,000 in damage not fully covered by their homeowner's deductible. They easily took a *withdrawal* from their UL cash value to cover the gap, as the initial loan interest didn't appeal to them in an immediate crisis. They understood that withdrawals reduce the death benefit and are permanent, but in that situation, it was the right choice.

- **Down payments for investment properties:** (expanding your real estate portfolio).

- **Mortgage payments during job loss or financial strain:** Policy loans don't require credit checks, they're non-callable as long as your policy stays active, and they're tax-free (assuming your policy isn't a MEC and stays in force). Withdrawals directly reduce your death benefit — they're permanent — and can be taxable if you pull out more than you've paid in premiums. Loans, though? Generally tax-free. IRC Sections 7702 and 7702A govern all this.

- **Educational expenses or retirement income:** The ability to take tax-free loans in retirement is a powerful feature known as "LIRP" (Life Insurance Retirement Plan), a strategy used by homeowners to create a supplementary income stream.

A Critical Mistake Homeowners Must Avoid

Flexible premiums don't mean you can skip payments or consistently pay only the minimum. I've seen policies lapse because homeowners, often during expensive renovations or financial stress, consistently underfunded their policies.

This is a death trap.

Remember that Scottsdale client? He'd been paying his UL policy for 15 years. Built up around $40,000 in cash value. Felt pretty secure. Then he started minimizing payments to the absolute bare minimum — wanted to free up cash for speculative property investments.

Here's what killed him: the cost of insurance charges increase every year as you age. Insurance companies use mortality tables (like the Commissioners Standard Ordinary tables) to calculate these charges. When you're 35, they're low. When you're 62? They're climbing fast.

So — his minimal payments couldn't keep pace with rising costs plus administrative fees (surrender charges, premium loads, expense loads — they all stack up). His cash value got eaten alive. Within three years, it dropped to zero. He got a 60-day notice that his policy would lapse unless he made a substantial payment.

He couldn't.

Lost the policy. Lost the $250,000 death benefit. Lost over $30,000 in premiums he'd already paid. Everything gone.

Don't rely on the minimum. Fund at or above the recommended premium, especially as you age.

Our 20+ Years of Professional Recommendation

For homeowners considering an IUL, **Penn Mutual** consistently delivers.

Why Penn Mutual? They don't chase flashy cap rates that sound great in sales meetings but rarely deliver. Instead, they focus on robust downside protection and guaranteed multipliers — exactly what homeowners need for secure, long-term growth.

They're a mutual company. That means no outside shareholders demanding quarterly profit spikes. Policyholders essentially own the thing. Any profits get redistributed back to you (dividends aren't guaranteed with IUL, but the structure shows where their priorities are). Their IUL products typically feature competitive cap and participation rates, sometimes with "uncapped" strategies or enhanced participation rates triggered by specific conditions.

The expense structure? Transparent. Actuarially sound. That stability makes their IULs reliable over 30-40 year timelines.

You might forgo some extreme upside potential, but you gain consistent and protected performance. In my experience, that's more valuable for homeowners planning decades ahead. I've seen this strategy pay off countless times, especially for clients in high-value markets near Seattle, like Bellevue and Mercer Island, where leveraging every financial tool is key.

Strategies Many Don't Share with Homeowners

Here's an undisclosed strategy: **overfund your IUL policy aggressively during the first 10-15 years**. This "front-loading" technique supercharges tax-deferred cash value growth.

You're creating a substantial financial reservoir you can access later — but you've got to stay under the Modified Endowment Contract (MEC) limit. IRC Section 7702A sets that limit to prevent policies from becoming "too rich" in cash value relative to their death benefit (which would strip away the tax advantages).

So yeah, you pay premiums significantly higher than your target — sometimes 2-3x higher — but you stay just below the MEC threshold. This maximizes compound interest and index crediting during the most efficient years of your policy.

Later, you can tap this cash value via tax-free loans. Some homeowners use this to pay off their entire mortgage decades early. True home security. This tactic, often referred to as "Be Your Own Bank" or "Infinite Banking," relies on the non-taxable nature of policy loans (assuming your policy isn't a MEC and stays active).

A couple in Buckhead (Atlanta) funded their IUL with $18,000/year for 12 years — well above their $8,400 target premium but below their MEC limit of $22,000. By year 15, their cash value hit $285,000. They started taking $35,000/year in tax-free loans to supplement their retirement income while their primary residence appreciated. The death benefit stayed intact for their heirs.

That's the play.

In-Depth Look

Detailed illustration of key concepts

Visual Guide

Infographic illustration for this topic

Side-by-Side Comparison

Visual comparison of options and alternatives

Sources & References

- IUL vs Universal Life: Choose The Right One For You

- Whole Life Insurance vs. Universal Life Insurance: Explained

- Indexed Universal Life (IUL) vs Whole Life Insurance - Ethos

- Compare and contrast: Indexed universal life vs. whole life insurance

- Indexed Universal Life vs. Whole Life Insurance | Progressive

- Building Codes, Standards, and Regulations: Frequently Asked ...

- Building Codes and Standards - 101 Guide | ROCKWOOL Blog

- Building Codes | NAHB

- Building Codes and Regulations - Illinois Capital Development Board

- Model Building Codes - Smart Home America

Frequently Asked Questions

Need Professional Help?

Find top-rated insurance services experts in your area