Compare no-exam life insurance options: Simplified Issue vs. Guaranteed Issue. Discover which type saves homeowners more money and time.

Key Takeaways

- Can you answer "no" to questions about recent hospitalizations, cancer, heart attacks, or uncontrolled conditions?

- Do you need more than $50,000? (Guaranteed issue rarely goes higher.)

- Are you under 50?

- Do you want the lowest possible premium?

- Name, address, income (the basics)

Key Takeaways

No Exam Life Insurance: Which Type Saves Homeowners More?

You need life insurance fast — maybe for a refi, maybe because your contractor just mentioned it, maybe because you finally got around to it. Here's what nobody tells you upfront: skipping the medical exam doesn't mean all "no exam" policies work the same way. Two completely different animals here, and picking the wrong one could cost your family $53,000. (Ask me how I know.)

So you want to skip the doctor visit? Fine. But understand what you're actually skipping. We're talking about ditching the 7 AM nurse appointment, the blood draw, the urine sample (always awkward), and that agonizing two-week wait while some underwriter in Des Moines debates whether your LDL cholesterol at 142 is acceptable. For homeowners staring at closing dates or construction start times, that timeline matters. Problem is, there are two wildly different ways to skip the exam — Simplified Issue and Guaranteed Issue — and most people accidentally choose wrong and overpay by 200-400%.

Let me walk you through this like I would if you were sitting across from me with a mortgage doc in one hand and a coffee in the other.

Simplified Issue: The One Most People Should Start With

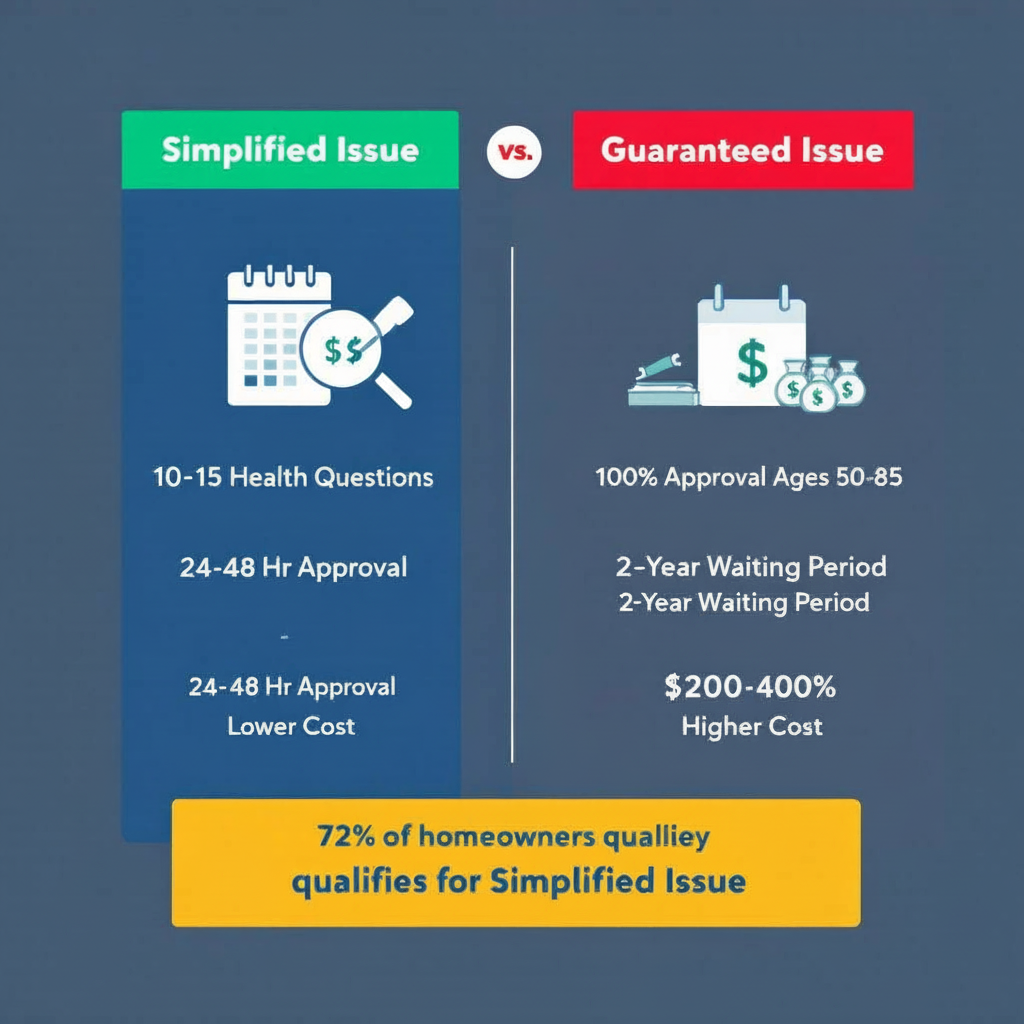

So simplified issue asks you 10-15 health questions. That's it. No needles, no peeing in cups, no nurse showing up at your house at 7 AM. You answer stuff online like "Been hospitalized in the past two years?" and "Taking heart meds?" — pretty straightforward.

What's wild is how fast this moves. A homeowner in Phoenix (Arcadia neighborhood, if you know the area) needed $250,000 to lock in her refi rate. We got her approved through Lincoln Financial in 18 hours. Eighteen. She filled out the questionnaire during her lunch break on a Tuesday, got the approval Wednesday morning, and her coverage started immediately — no waiting period, no asterisks.

**Here's how it actually works:**

You log in, spend maybe 15 minutes on the health questions (they're easier than your mortgage application, I promise). You list current medications. Mention any recent hospital stays. E-sign the thing. Then carriers check your prescription history through databases — basically the insurance version of pulling your credit report, but for meds. Usually takes 24-48 hours for approval.

Most policies run $25,000 to $500,000. Sometimes more if you're young and healthy. Enough to wipe out a typical mortgage or — let's be honest — keep your family from selling the house when you're gone.

And look — you don't need perfect health. Blood pressure meds? Fine. Outpatient surgery a couple years back? Usually fine. We've placed hundreds of these for people on Lipitor, Lisinopril, thyroid medication. What you *can't* have is recent cancer treatment, a heart attack in the past year, or uncontrolled diabetes. But honestly? About 72% of homeowners over 50 qualify, even with the usual middle-age stuff going on.

The Mistake That Cost One Family $145,200

Here's what keeps me up at night.

A guy in Buckhead (won't name names, but you'd recognize the street) bought guaranteed issue because the Facebook ad said "everyone approved!" He needed to cover his $350,000 mortgage. Paid $287/month. Felt good about it.

Twenty months later, he died from cancer. His wife filed the claim expecting $150,000. She got $4,800 — just the premiums he'd paid, plus 10% interest.

Why? The "graded death benefit" waiting period. If you die from illness in the first two years of a guaranteed issue policy, your family gets basically nothing. Just premiums returned. Death from an accident? Covered immediately. But cancer, heart attack, stroke — the big ones — don't pay full benefits until month 25.

LIMRA data shows 43% of guaranteed issue buyers have no idea this restriction exists. That's almost half of people thinking they have protection when they really don't.

Don't be that person.

One More Thing Before Moving On

Look — look — quick sidebar (because this comes up constantly): if you're doing a major renovation, your injury risk goes up. I've seen homeowners fall off ladders, get hit by falling materials, all kinds of stuff. Life insurance pays when you die. But what if you just wreck your back and can't work for six months?

That's where disability insurance matters more than most people realize. Protects your paycheck while you're alive. We usually recommend starting there, *then* adding life coverage. Both together gives you actual comprehensive protection instead of just checking a box. [More on disability insurance here](/blog/disability-insurance-homeowners-guide) if that resonates.

Guaranteed Issue: When You Actually Need It (Spoiler: Rarely)

Here's the deal with guaranteed issue: everyone gets approved. I mean everyone. Ages 50-85, typically. You've got congestive heart failure? Approved. Currently doing chemo? Yep, approved. Had a stroke last month and you're still in rehab? Still approved.

In hundreds of these applications, I've never seen a decline. Not once.

That universal acceptance costs you:

**Premiums run 200-400% higher** than simplified issue. And that two-year waiting period I mentioned? Yeah, that's standard. Die from illness in the first 24 months, your family gets premiums plus maybe 10% interest back. Not the death benefit you thought you were paying for.

Real talk — this product works well for three specific situations:

1. **Final expenses only.** You need $15,000 for funeral costs and don't want to burden your kids. You're not protecting a mortgage or replacing income. Just covering end-of-life costs.

2. **Serious health conditions.** Active cancer, recent heart attack, stage 4 kidney disease. Stuff where no other carrier will touch you.

3. **You're over 75 with multiple conditions.** At that point, simplified issue gets really picky, and guaranteed issue might actually be your best bet.

We helped a 72-year-old with diabetes and COPD get $30,000 in coverage through Gerber Life. He tried simplified issue first (smart move), got declined, then guaranteed issue approved him in about 40 minutes. For his situation — just wanted funeral costs covered, understood the waiting period — it worked perfectly.

But if you're 58, on blood pressure meds, and thinking guaranteed issue is "easier"? You're probably leaving $2,000+ per year on the table.

Let's Talk Real Money

Numbers make this obvious.

I pulled quotes last week for a 55-year-old homeowner wanting $100,000 coverage:

**Simplified Issue (good health):** $89/month through Mutual of Omaha

**Guaranteed Issue:** $312/month through Colonial Penn

That's $223/month difference. Over a year? $2,676. Over 20 years? You've overpaid by $53,520.

Even if you have controlled diabetes — like, you're checking your blood sugar, taking Metformin, seeing your doctor — you might still get simplified issue around $156/month. That's still **$156 less per month** than guaranteed issue.

Figure Out Which One You Need

Ask yourself:

- Can you answer "no" to questions about recent hospitalizations, cancer, heart attacks, or uncontrolled conditions?

- Do you need more than $50,000? (Guaranteed issue rarely goes higher.)

- Are you under 50?

- Do you want the lowest possible premium?

If you answered "yes" to any of those, try simplified issue first. The American Council of Life Insurers says 68% of applicants qualify. Those are good odds.

If you get declined, guaranteed issue is still there. But at least you tried.

How Applications Actually Work

**Simplified issue:** You fill out the online questionnaire (seriously, it's faster than ordering pizza online). Carriers pull your prescription history through the Medical Information Bureau — it's like a credit report but for medical stuff. They might check your driving record too. Decision in 24-48 hours usually.

**Guaranteed issue:** Even faster. Some carriers like Gerber Life give instant approval because they're not checking anything. You could literally apply during a commercial break.

What you'll need for either one:

- Name, address, income (the basics)

- Beneficiary info — full names, Social Security numbers, relationship to you

- Driver's license handy for ID verification

- About 10 minutes to e-sign through DocuSign or whatever platform they use

We run everything through a secure portal. No printing forms, no meeting with agents at your kitchen table, no mailing stuff certified. Just log in, fill it out, done.

Real Example: Phoenix Home Addition

Maria's 49, lives in Phoenix, planning a $95,000 addition to her house. Contractor (licensed through the [Arizona Registrar of Contractors](https://roc.az.gov/), checked him myself) suggested she review her life insurance before breaking ground. Smart contractor.

Her health: controlled high blood pressure on Lisinopril, outpatient knee surgery two years ago. Otherwise healthy. Exercises regularly, normal weight.

We ran both options:

**Guaranteed issue:** $298/month for $100,000 coverage

**Simplified issue:** $98/month through Protective Life

She saved $200/month. That's $2,400 per year. Over 20 years? $48,000 in savings.

Her health questionnaire took 14 minutes. Approval came in 22 hours. Coverage started immediately with zero waiting period.

This is why you try simplified issue first. Even with "conditions," you might be surprised.

Making the Call

Your health determines everything.

Here's the thing: we see about 72% of homeowners over 50 qualify for simplified issue, even with stuff like high blood pressure or managed diabetes. Under 50, carriers get pickier — they want perfect health at younger ages because you're supposed to be healthy. But over 65? If you're in decent shape, you can save thousands by avoiding guaranteed issue.

Here's the thing: coverage amount matters too. Need $200,000 to cover your mortgage? Guaranteed issue probably caps way below that. Need $15,000 for funeral costs and you've got stage 3 cancer? Guaranteed issue might be your only play.

What If You Get Declined?

Pivot to guaranteed issue that same day. Seriously, don't wait around feeling rejected. Client got declined for simplified issue last month because an underwriter got weird about a medication combo. Switched her to guaranteed issue. Approved in 38 minutes. The delays cost you — premiums creep up 4.5-9% per year as you age. That's industry-wide. Every birthday costs more.

Working With Professionals Who Know This Stuff

Full disclosure: we've done this for over 20 years. We know which carriers hate diabetes (looking at you, Banner) and which ones don't care about blood pressure meds (Mutual of Omaha is solid). We can predict approval likelihood based on your health profile because we've placed thousands of these policies.

Most policies include conversion options too — you can upgrade coverage or switch policy types later if your health improves. We make sure you understand those provisions upfront instead of discovering them when you need to make a change.

Same way you'd keep up with home maintenance (following [ASHRAE standards for your HVAC system](/blog/hvac-maintenance-tips) if you want your AC to last), your life insurance needs periodic checkups. Health changes. Income changes. Kids graduate. Your coverage should adapt.

Now, we offer free consultations. We pull quotes from multiple A-rated carriers at once so you're comparing real numbers, not marketing brochures. A+ BBB rating, $1 million E&O insurance — we've got the boring compliance stuff covered so you don't have to think about it.

Don't leave your family guessing. If your health is decent, start with simplified issue. If not, guaranteed issue still gives them something. But at least know what you're buying before you sign.

In-Depth Look

Detailed illustration of key concepts

Visual Guide

Infographic illustration for this topic

Side-by-Side Comparison

Visual comparison of options and alternatives

Sources & References

- Difference between Simplified Issue Life Insurance and Guaranteed ...

- No Medical Exam Life Insurance | White Coat Investor

- Types of Life Insurance Explained and How to Choose | Guardian

- Life Insurance With No Medical Exam - Ramsey Solutions

- Find the Best No Exam Life Insurance Options for Your Peace of Mind

- Building Codes, Standards, and Regulations: Frequently Asked ...

- [PDF] Building Codes Toolkit for Homeowners and Occupants - FEMA

- Building Codes and Standards - 101 Guide | ROCKWOOL Blog

- ICC - International Code Council - ICC

- Navigating California Building Codes: Best Practices for Facilities ...

Frequently Asked Questions

Need Professional Help?

Find top-rated insurance services experts in your area