Young adults can save up to 70% on life insurance premiums by starting in their 20s. Lock in lower rates and secure your financial future.

Key Takeaways

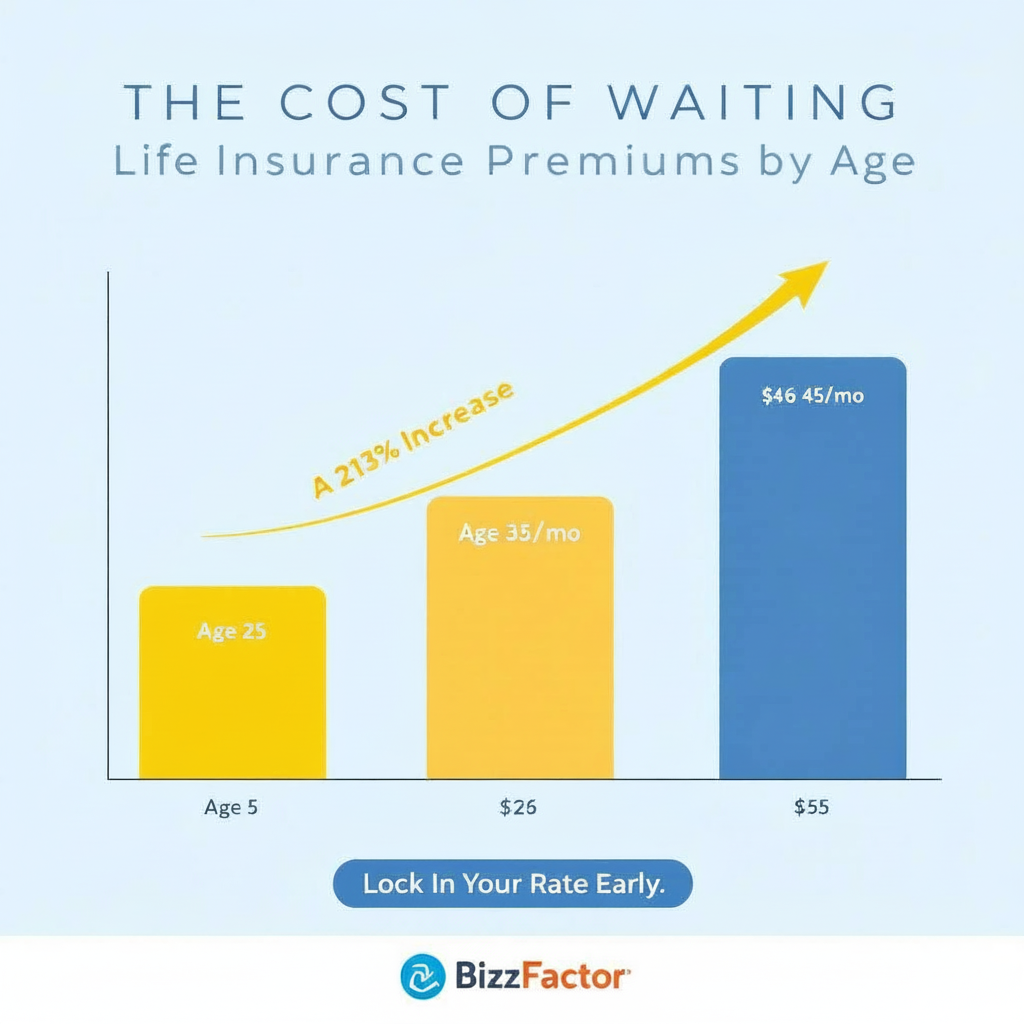

- **Age 25**: Approximately $16/month for $500,000 in coverage.

- **Age 35**: The premium rises to about $26/month (a 63% increase from age 25).

- **Age 45**: The cost escalates to roughly $50/month (a substantial 213% increase compared to age 25).

- **Brother A**, proactive and informed, purchased $750,000 in protection at age 28. His monthly premium is $38.

- **Brother B**, who delayed, secured the same coverage at age 38. His monthly cost is $65.

Key Takeaways

Life Insurance for Young Adults: Save 70% Starting in Your 20s

Securing life insurance in your twenties isn't just about foresight; it's a strategic financial move that can slash your premiums by up to 70% compared to delaying. For instance, a healthy 25-year-old might pay a mere $16 monthly for substantial coverage that could cost upwards of $50 by the time they reach their 40s. At BizzFactor, we've guided thousands of young individuals in locking in these advantageous rates, ensuring their financial futures are protected.

Why Does Early Coverage Create Massive Life Insurance Savings?

Look — look — here's what most people don't get about life insurance pricing. Your premium gets locked in based on your age when you apply. That's the real issue. Once the policy's issued, that rate sticks — doesn't matter if you gain weight, develop diabetes, or age another decade. That's it. That permanency is everything.

I've sat across from hundreds of 35-year-olds who kicked themselves for waiting. The math isn't subtle. A healthy 25-year-old getting a $500,000, 20-year term policy? Around $16 a month. That same person at 45? They're looking at $50 monthly.

213% increase.

Same person. Same health (hopefully). Drastically different price tag just because they waited.

We recently advised a young couple purchasing their first home. By integrating life insurance into their financial planning alongside their homeowner's protection, they made a remarkably astute decision. The husband, at 28, secured $750,000 in coverage for just $38 monthly. That's the real issue. This proactive approach not only protected their new asset but also their future financial stability.

From an actuarial standpoint, you're less likely to die young. Sounds morbid, but that's the math. Insurance companies price based on risk tables — the younger and healthier you're, the cheaper your coverage. They're literally betting you'll pay premiums for decades before they pay out a dime.

Beyond just premiums, there's a vital feature often overlooked: **conversion privileges**. This often-understated benefit can be more valuable than the initial low premium itself.

What's a Conversion Privilege in Life Insurance?

Here's the thing: here's the thing: so let's say you buy term insurance at 25. Ten years later, you're diagnosed with something serious — high blood pressure, pre-diabetes, whatever. Normally, you'd be screwed trying to get new coverage.

But here's where conversion privileges save your ass: you can flip that term policy into a permanent one (whole life, universal life, etc.) **without any medical exam or health questions**. Zero. They can't ask about your current health status because the conversion right was built into your original contract.

Why does this matter so much?

Health changes fast. I've watched clients in their mid-30s get diagnosed with Type 2 diabetes, heart conditions, even cancer. Without a conversion option built into their original term policy, they're either uninsurable or facing premiums that'd make you cry. A guy I worked with in Buckhead — 37 years old, developed a heart condition — tried getting new coverage and got quoted $340/month for what used to cost him $45. His old policy had no conversion rights.

He was stuck.

Always — and I mean always — confirm these conversion options before signing anything. It's buried in the fine print, but it's probably the most valuable feature your policy has (besides, you know, actually paying out when you die).

Real talk — to learn more about secure financial planning, consider exploring our resources on [asset protection strategies](https://www.bizzfactor.com/asset-protection) and [retirement planning basics](https://www.bizzfactor.com/retirement-planning).

How Much Do You Really Save by Starting Life Insurance Early?

I've run the numbers on this probably two hundred times for clients. Here's what happens when you wait:

- **Age 25**: Approximately $16/month for $500,000 in coverage.

- **Age 35**: The premium rises to about $26/month (a 63% increase from age 25).

- **Age 45**: The cost escalates to roughly $50/month (a substantial 213% increase compared to age 25).

And it gets worse with bigger policies. A $1 million policy that might cost $30 monthly at 25 could jump to $100 monthly at 45. That's an additional $70 every month for 20 years, totaling an extra $16,800 in avoidable costs. Don't skip this. I've seen this pattern repeat itself across hundreds of client analyses: waiting longer invariably means paying exponentially more.

Real Client Example: The Cost of Waiting

Consider the case of twin brothers, both engineers with similar health profiles, but with different approaches to life insurance timing.

- **Brother A**, proactive and informed, purchased $750,000 in protection at age 28. His monthly premium is $38.

- **Brother B**, who delayed, secured the same coverage at age 38. His monthly cost is $65.

The math is brutal: Brother B pays an extra $324 every year. Over 20 years? That's $6,480 thrown away for being ten years late. Same coverage, same health, drastically different cost.

What About Young Adults Without Dependents?

So yeah, I get asked this constantly: "Why do I need life insurance if I'm single and have no dependents?" Fair question. But here's what you're probably not thinking about:

**Student loans don't die with you.** Neither do car loans, credit cards, or that personal loan your mom co-signed. Those balances? They land on whoever's left — usually your parents or siblings. I've seen families get hit with $60,000+ in debt after losing someone. That's not a legacy anyone wants to leave.

**Your health today means nothing tomorrow.** You could be running marathons right now and get diagnosed with something next year. Once that happens, getting affordable coverage (or any coverage) becomes nearly impossible. Locking in a policy while you're healthy guarantees you're insurable no matter what.

**Single doesn't last forever.** Most people eventually partner up, get married, maybe have kids. When that happens, you need coverage immediately — but you won't want to wait 4-6 weeks for underwriting when you've got a newborn at home.

Last year I helped a 26-year-old teacher in Decatur set up her first policy. Single, no kids, renting an apartment. But she had $45,000 in student loans co-signed by her parents.

She got a $250,000 policy for $18/month.

Her logic? "If something happens to me, I don't want my parents inheriting my debt on top of losing their daughter." That's the kind of thinking that separates people who plan ahead from people who leave messes behind. It matters more than you'd think. This illustrates how life insurance protects more than just dependents; it safeguards your estate and family from unexpected liabilities. For further financial guidance, explore our articles on [managing student debt](https://www.bizzfactor.com/student-loan-management) and [building generational wealth](https://www.bizzfactor.com/generational-wealth).

How Does the "Laddering" Strategy Work for Life Insurance?

Here's what smart planners do instead of buying one massive 30-year policy: they ladder. Basically, you're buying multiple smaller policies with different end dates. Something like:

- A $200,000 policy for 10 years

- Another $200,000 policy for 20 years

- A $100,000 policy for 30 years

So — the logic? Your needs change. Maybe in 10 years you've paid off your student loans — cool, let that first policy expire. In 20 years, the mortgage is gone. Now you're only maintaining the 30-year policy for final expenses and legacy planning. You're not overpaying for coverage you don't need anymore, which is exactly what happens with those one-size-fits-all policies most people buy.

What Questions Should You Ask Life Insurance Agents?

Don't just take the first quote someone throws at you. Shop around. Compare at least three carriers. And when you're talking to agents, ask these questions — write down their answers:

- **"What are the specific conversion options available?"**: Demand detailed information in writing. Understand which permanent products you can convert to and any deadlines for conversion.

- **"What's the company's financial rating?"**: Look for A+ ratings from A.M. Best, Standard & Poor's, Moody's, or Fitch. You're betting this company will be around in 30 years to pay out — make sure they're financially solid.

- **"Can I increase coverage later without additional medical exams?"**: Inquire about guaranteed insurability riders. While they may add a small cost, they offer invaluable flexibility to increase coverage as life events dictate, without proving current health.

- **"What happens if I miss a premium payment?"**: Understand the grace period and the implications of missed payments to ensure you know your policy's safety net.

Red Flags to Avoid When Choosing an Agent

I've seen too many people get burned by pushy agents who care more about their commission check than your actual needs. Watch out for:

- **Pressure for immediate decisions**: Quality financial planning takes time and careful consideration. Hasty decisions are often poor decisions.

- **Promises that seem too good to be true**: If it sounds implausible, it likely is.

- **Inability to clearly explain policy details**: A competent agent should simplify complex terms and ensure you fully understand your policy.

- **Reluctance to provide written comparisons**: Always request and review side-by-side comparisons of different policies and companies.

- **Pushing only one insurance company**: A truly independent agent will offer options from multiple carriers to find the best fit for your unique needs.

Like selecting a contractor for [kitchen-bath-remodeling](https://www.bizzfactor.com/kitchen-bath-remodeling) or [HVAC services](https://www.bizzfactor.com/hvac-services), quality insurance guidance demands expertise, transparency, and patience. If they're rushing you, walk away.

When Should You Actually Apply for Life Insurance?

Simply put: **Right now**, assuming you're healthy and in your 20s or 30s. Each month you postpone risks higher premiums, and every shift in your health status jeopardizes your insurability. Your actionable strategy should include:

1. **Calculate your actual needs**: Systematically sum up all current debts, necessary income replacement for dependents, and future financial obligations.

2. **Obtain multiple quotes**: Compare at least three reputable, A-rated insurance providers to ensure competitive pricing and comprehensive coverage.

3. **Schedule medical exams promptly**: The underwriting process typically takes 4-6 weeks, so quick action here can prevent delays.

4. **Consider convertible term coverage**: This offers the essential flexibility to adapt your policy as your life circumstances evolve.

5. **Review annually**: Your life is dynamic; your coverage should be too. Regular reviews ensure your policy remains aligned with your current needs.

The Life Insurance Application Process: What to Expect

Our BizzFactor team streamlines this process, guiding clients through each step. Here's a typical timeline:

- **Week 1**: Complete the application and schedule your medical examination.

- **Weeks 2-4**: The underwriting team reviews your medical records and verifies financial information.

- **Weeks 4-6**: A final decision is made, and your policy documents are delivered.

Crucially, many insurers provide temporary coverage during the underwriting period, offering immediate protection while your application is finalized.

How Does Life Insurance Connect to Overall Financial Protection?

Look — think abo

In-Depth Look

Detailed illustration of key concepts

Visual Guide

Infographic illustration for this topic

Side-by-Side Comparison

Visual comparison of options and alternatives

Sources & References

- Life Insurance for Young Adults: Why Starting Early Saves Thousands

- 5 Things To Know About Life Insurance in Your 20s and 30s

- The Importance of Life Insurance: Why Getting It in Your 20s and 30s ...

- Life Insurance in Your 20s or 30s - Drucker Wealth Management

- Building Codes, Standards, and Regulations: Frequently Asked ...

- Building Codes and Standards - 101 Guide | ROCKWOOL Blog

- [PDF] Building Codes Toolkit for Homeowners and Occupants - FEMA

- ICC - International Code Council - ICC

- Home Insurance Building Code Coverage - Allstate

Frequently Asked Questions

Need Professional Help?

Find top-rated kitchen & bath remodeling experts in your area