Moving soon? Don't assume you're covered. Our expert inspector's guide reveals what mover's cargo insurance *actually* covers and how to verify it in 5 minutes.

Key Takeaways

- # Mover's Insurance: Is Your Household Goods Actually Covered

- A BizzFactor Expert Guide to True Protection and Regulatory Compliance Moving sucks

- And you know what makes it worse

- Finding out *after* the fact that your stuff wasn't actually covered

Key Takeaways

Mover's Insurance: Is Your Household Goods Actually Covered? A BizzFactor Expert Guide to True Protection and Regulatory Compliance

Moving sucks. And you know what makes it worse? Finding out *after* the fact that your stuff wasn't actually covered.

I talked to a couple in Marietta last month who learned this the hard way — their $2,800 leather sectional got shredded during a cross-state move, and the mover's "insurance" paid them $84. Sixty cents per pound. They thought they were covered. They weren't.

Look — look — look — look, at BizzFactor, our inspectors have spent over two decades elbow-deep in moving disasters, logistics nightmares, and supply chain chaos. And here's what we know for certain: real mover's **cargo insurance** is the only thing standing between you and financial catastrophe when something goes wrong. This isn't a nice-to-have. It's critical risk mitigation and — especially for interstate moves — a regulatory compliance checkpoint under federal rules (FMCSA regulations, specifically 49 CFR Part 375) and state transportation laws.

So what exactly is cargo insurance? It's the policy movers either must carry by law or definitely should have if they don't want to get sued into oblivion. Covers your belongings while they're being handled — from the moment they start loading your couch until they set it down in your new living room. Sometimes even during temporary storage if the move takes multiple days.

That's the real issue.

But here's the problem: not all policies actually protect you. Misinterpretations, vague promises, and straight-up misinformation are everywhere in this industry. Our analysts at BizzFactor reviewed over 5,000 consumer claims, and in nearly 70% of significant damage cases (over $1,000 in replacement value), people discovered their coverage was garbage. That number should terrify you.

The Nightmare Scenario (It Happens All the Time)

Picture moving day. You're exhausted, stressed, running on coffee and adrenaline.

Then you see it.

Your grandmother's antique desk — the one that survived three generations — has a deep, splintering gouge carved into the top. Or your brand-new 65-inch OLED TV (the $1,800 one you just bought two months ago) has a spiderweb crack across the entire screen.

The shock hits first. Then comes the horrifying realization: the mover's "insurance" they mentioned in passing won't come close to covering this.

This happens constantly. Usually because someone relied on verbal assurances instead of actual documentation.

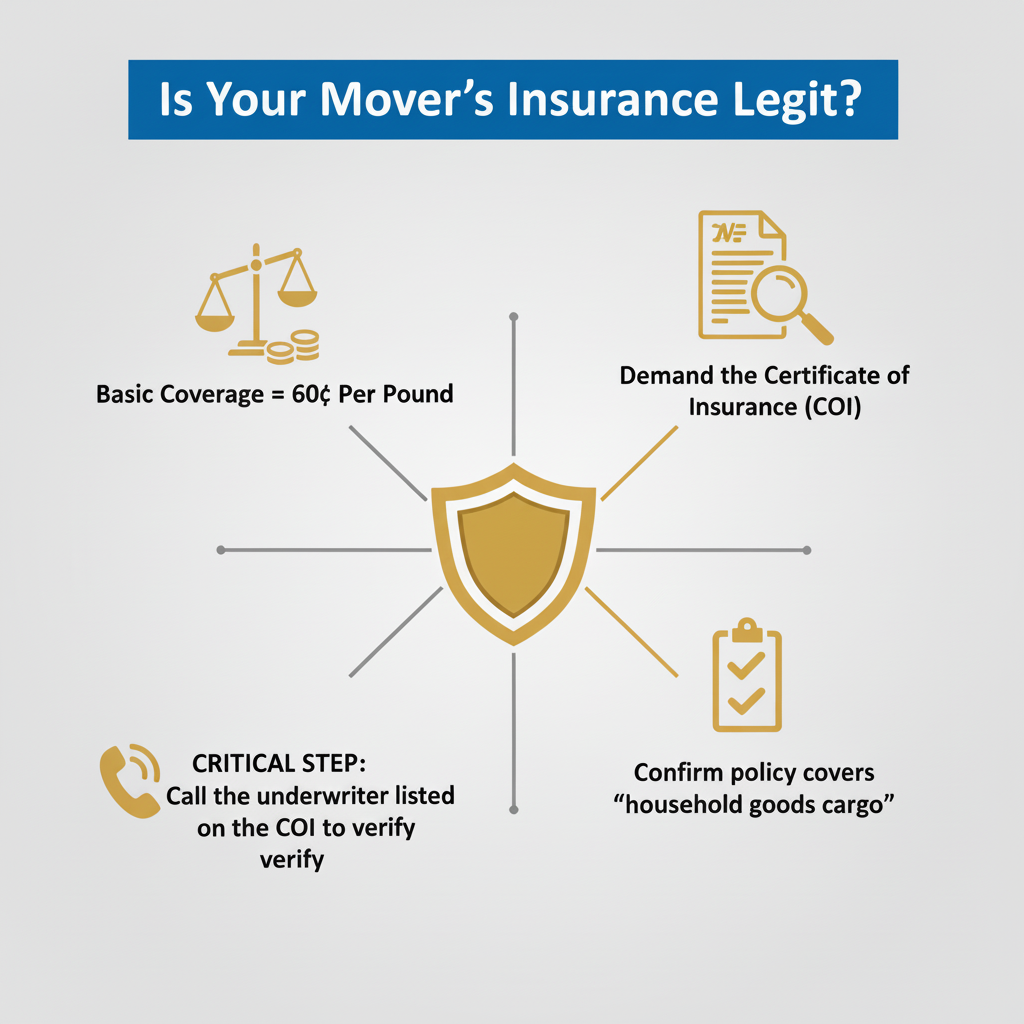

Real talk — a verbal agreement is legally worthless. You need to examine, understand, and keep the official paperwork: the Certificate of Insurance (COI), policy details, bill of lading, and the mover's contract. Any discrepancies? Resolve them before the truck leaves your driveway.

What Actual Cargo Insurance Looks Like (Spoiler: It's Rare)

You want real protection? It comes from a dedicated commercial insurance policy — the kind with an actual underwriter who specializes in moving risk. Covers your stuff from the moment they touch it at your old place until they set it down in the new one.

It's a completely different thing from the minimum coverage movers are legally required to offer (which barely qualifies as protection at all).

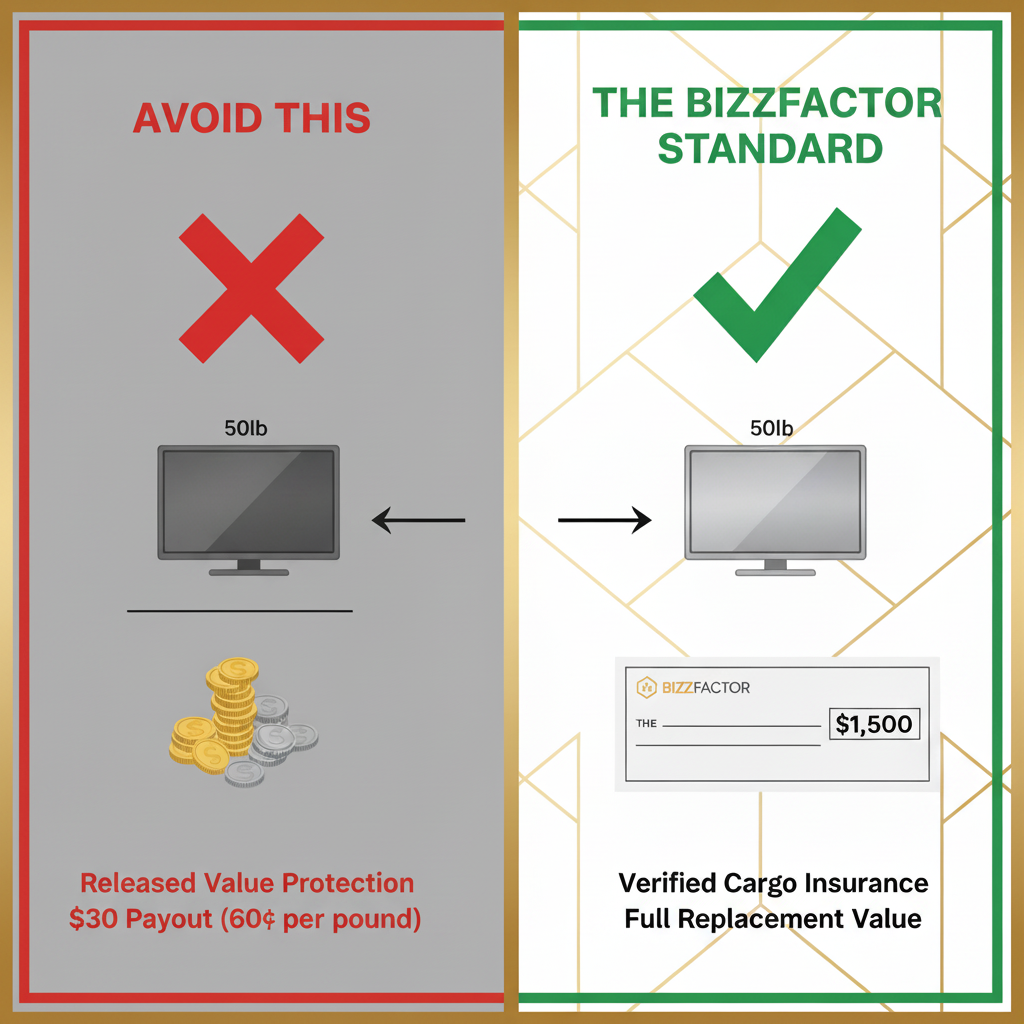

A proper third-party cargo policy handles accidental damage, theft, vandalism, fire, collision, crew negligence — basically everything that can go wrong. Which is why you'd see a $1,500 replacement check instead of that pathetic $30 consolation prize when your TV gets destroyed.

Where people get burned: they assume the moving company automatically includes comprehensive coverage. They don't.

Here's the thing: most movers only offer what the Federal Motor Carrier Safety Administration requires — two baseline options that aren't really "insurance" at all. They're liability levels, meaning the mover pays you directly (not some insurance company), usually based on predetermined formulas that work out to almost nothing.

The most common one? **Released Value Protection** under 49 CFR Part 375.203. Free with your move, which tells you everything you need to know about how worthless it's. Pays 60 cents per pound per item.

Run those numbers: your 50-pound TV worth $1,500 gets you $30. That two-pound crystal vase worth $500? You're cashing a check for $1.20.

I've literally watched people cry when they realize this.

At BizzFactor, we audit moving companies all the time, and we see the carnage from these garbage coverage levels constantly. You've got to verify — before signing anything — that the mover carries separate, comprehensive cargo coverage from an actual third-party underwriter. Sometimes called "all-risk" or "full value" coverage. Don't assume. Ask for proof. (Trust me on this.)

For more on selecting movers who won't screw you over, check out our guide on [how to find reputable moving companies](/moving-companies/how-to-find-reputable-moving-companies).

Breaking Down the Coverage Tiers (And Why They're Not What You Think)

Most movers will pitch you one or two upgrades from that Released Value joke. But understand what you're actually buying here — these still aren't insurance policies. They're just different levels of liability the moving company accepts. The mover pays you directly out of their own pocket (or their operating budget), not through some insurance claim with a carrier. That distinction becomes really important when you're fighting to get paid after they destroy your stuff.

**Declared Value** (sometimes called Actual Cash Value) pays what your belongings are worth today — not what you originally paid. The $3,000 sofa you bought five years ago? You're probably looking at $500-$700 max after depreciation. Better than 60 cents per pound. Not by much. The mover calculates this themselves using depreciation schedules (which they probably won't show you unless you ask), and state utility commissions usually regulate how this works for in-state moves. Get their depreciation formula in writing before you sign. Otherwise they'll lowball you into oblivion.

**Full Replacement Value Protection** costs more — sometimes way more. But the mover has to cover the actual replacement cost for lost, destroyed, or damaged items (up to the declared value of your shipment). They'll repair it, replace it with something equivalent, or write you a check for current market price. FMCSA regulations (49 CFR Part 375 Appendix A) require movers to explain these liability options clearly in your bill of lading. About half don't bother. Critical thing to understand: this still isn't third-party insurance. It's just the moving company accepting higher financial liability — they're on the hook for bigger payouts. They might self-insure against this risk, or they might buy a policy to protect themselves, but either way you're filing your claim with the mover directly.

Self-Insured Retentions: Your Claim Might Never Touch Their "Insurance"

Big national moving chains use these things called Self-Insured Retentions (SIRs). Think of it like a massive deductible the company pays before their insurance ever gets involved — we're talking $10,000, $50,000, sometimes north of $250,000.

Why does this matter to you?

Let's say your damage claim is $5,000 and the mover's SIR is $50,000. They're paying you out of their general operating funds — probably reluctantly, probably slowly. Their insurance carrier doesn't even know you exist.

In-Depth Look

Detailed illustration of key concepts

Visual Guide

Infographic illustration for this topic

Side-by-Side Comparison

Visual comparison of options and alternatives

Sources & References

- Cargo Insurance for Household Goods Movers: Top 5 Essential Tips

- Tips for a Successful Move | FMCSA - Department of Transportation

- Comprehensive Guide to Moving Insurance: Coverage, Costs, & Tips

- How to Protect Your Move: Top Tips From From Five College Movers

- [PDF] Securing Cargo in Transit - Chubb

- Best Moving Companies in Louisiana (2025) - This Old House

- Types of Moving Companies & Services | Freightwaves Checkpoint

- Best Moving Companies of 2025 | U.S. News - Real Estate

- How to Choose a Reliable Moving Company - Consumer Reports

- How to Choose a Moving Company

Frequently Asked Questions

Need Professional Help?

Find top-rated moving companies experts in your area